Why would you keep paying for a $1,000,000 policy in 2045 when your mortgage is settled and your kids are independent? Most visitors we help feel that life insurance must be a static, high cost burden for thirty years. We agree that paying for coverage you won’t need in two decades is a waste of your money. That’s where life insurance laddering comes in. This strategy allows you to layer multiple policies that expire as your financial responsibilities decrease, which can reduce your total premium costs by 25% or more over the life of the plans.

We’ll show you exactly how to match specific policies to your debts so you never overpay. You’ll get a clear roadmap for building a ladder that evolves with your family. Best of all, we make the research process stress free. You can get instant term life quotes on our site without entering your name, phone number, or email address. For other products like whole life or disability insurance, we ask for contact info up front. We believe it’s vital to have a real discussion with prospects before quoting those options to ensure accuracy. Read on to see how simple it is to secure your future while protecting your privacy.

Key Takeaways

- Discover how to align your coverage with your evolving financial needs so you aren’t paying for protection you no longer require as your debts decrease.

- Learn the strategic “three-rung” approach to life insurance laddering that allows you to layer policies for maximum savings and flexibility.

- Find out why a single large policy often leads to “wasted premiums” and how a custom ladder can significantly lower your total long-term costs.

- Use our step-by-step method to calculate your specific rungs based on your current debt obligations and family income replacement goals.

- See how we provide instant term quotes anonymously, though we require contact info up front for other products so we can have a discussion with you before quoting.

What is Life Insurance Laddering and How Does It Work?

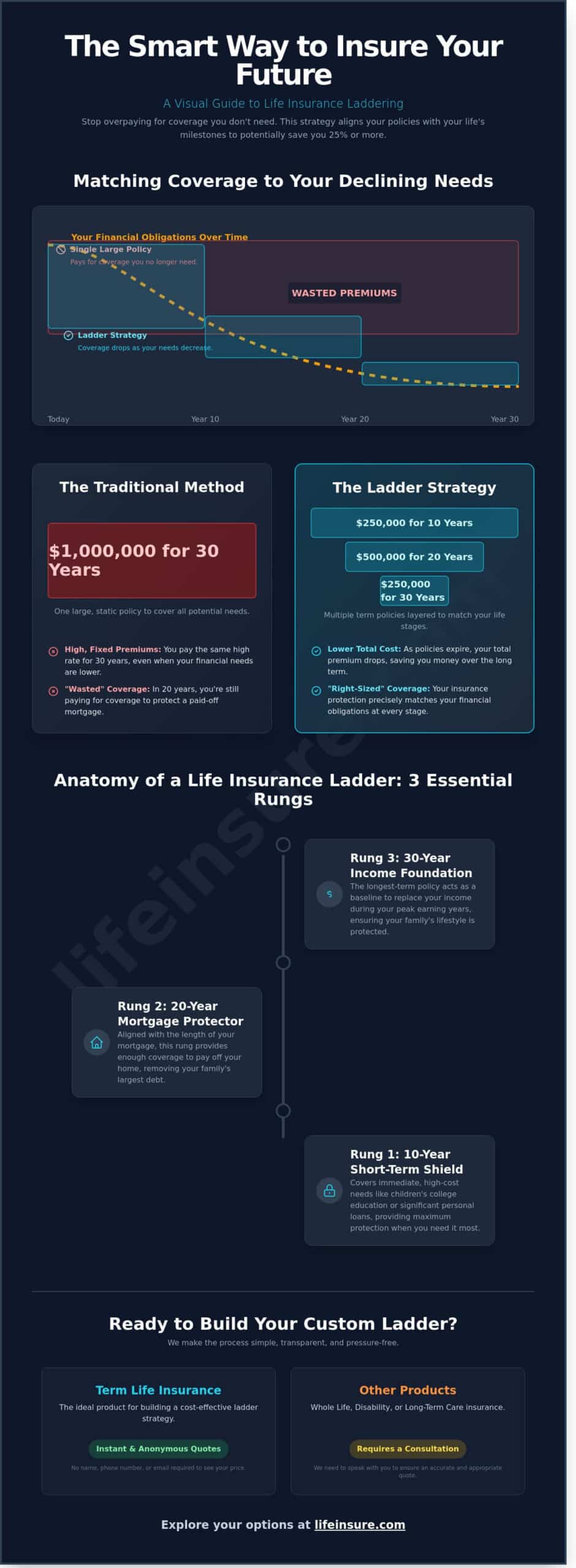

Life insurance laddering is a strategic way to structure your protection by layering multiple policies with different expiration dates. Instead of buying one massive 30-year term policy to cover everything, you buy several smaller policies that expire as your financial obligations disappear. We call these “rungs” on your ladder. Each rung represents a specific milestone, such as your children graduating college or your mortgage being paid off. This method ensures you aren’t paying for high levels of coverage you no longer need in your 50s or 60s.

The core logic is simple. Your financial needs are usually at their peak right now. You might have a new home, young children, and decades of lost income to replace. As time passes, your mortgage balance drops and your savings grow. By using Term life insurance in staggered layers, you match your coverage to this natural decline in debt. We help visitors visualize this downward slope so they can stop overpaying for “max-sized” plans that don’t fit their actual timeline.

The Financial Philosophy Behind the Ladder

We view insurance as a temporary financial bridge, not a permanent burden. Most liabilities have a clear expiration date. A 20-year mortgage will eventually be zero. A child will eventually finish their 17th year of schooling and enter the workforce. Because these costs disappear, your insurance should too. We focus on “right-sized” coverage. This philosophy prevents prospects from being over-insured in their later years. It allows you to redirect those saved premiums into your retirement accounts or 5200 college savings plans where the money can actually grow for you.

Why Laddering is More Relevant in 2026

Precision matters more than ever in 2026. With average mortgage rates hovering around 6.4% and the cost of living remaining a primary concern for families, every dollar in your budget must work hard. Modern life insurance policies now allow for much more granular customization than they did a decade ago. We advocate for a tailored approach because it’s more efficient. It’s easier to manage three specific rungs than one giant, expensive policy that covers risks you won’t have in 15 years.

We make it easy to explore these options. Visitors can get term life insurance quotes on our site instantly without providing a name, phone number, or email address. We want you to see the savings for yourself without any pressure. If you are interested in other products like whole life, disability insurance, or long-term care, we do require contact information up front. This is because we need to have a discussion with a prospect before quoting them to ensure the policy meets their specific health and financial profile. Whether you want a simple quote or a deep dive into a laddering strategy, we are here to guide you through the process.

The Anatomy of a Life Insurance Ladder: 3 Essential Rungs

We view a successful financial strategy as a structure built to weather the different seasons of your life. By using term life insurance as the primary building block, we can help you layer coverage to match specific financial obligations. According to CBS News, laddering your life insurance allows you to avoid paying for high coverage amounts you won’t need 20 or 30 years from now. This approach breaks down your protection into three distinct time horizons: short, medium, and long-term. Each rung targets a specific pain point that prospects face as they grow their families and careers.

Rung 1: The 10-Year Short-Term Shield

This first layer addresses your most immediate, high-cost debts. We often suggest this rung for prospects managing personal loans or those with children who are about 12 years old and nearing their college years. You don’t need a 30-year policy to cover a 10-year tuition window. This rung provides a massive boost in coverage when your family is most vulnerable. It’s the most cost-effective rung to add to an existing plan because the shorter duration keeps premiums low while providing maximum protection during those critical high-spending years.

Rung 2: The 20-Year Mortgage Protector

Your home is likely your largest asset. We align this policy length with the remaining duration of a standard home loan. If you’re 10 years into a 30-year mortgage, a 20-year rung ensures your family stays in their home if the primary earner passes away. This specific layer offers immense psychological peace of mind for visitors. There’s a unique sense of relief that comes from knowing the “roof over their heads” is secured by a dedicated policy. It simplifies your planning by matching the debt’s life cycle exactly to the insurance term.

Rung 3: The 30-Year or Permanent Foundation

The final rung covers your longest-lasting needs, such as a spouse’s retirement income or final expenses. This is the foundation of your life insurance laddering strategy. While you can get instant term life insurance quotes on our site without entering your name, phone number, or email address, permanent options work differently. For a permanent foundation, we require you to provide contact information up front.

We do this because we need to have a discussion with a prospect before quoting them on permanent products. We want to ensure the policy meets your long-term cash value goals and tax planning needs. While term quotes are instant and private, this permanent foundation often requires our expert guidance to get right. If you’re looking for coverage that lasts a lifetime, you can request a permanent insurance consultation to speak with an experienced agent who will stay with you from start to finish.

Laddering vs. A Single Large Policy: A Cost-Benefit Analysis

Choosing between one large policy and a laddered strategy often comes down to how much you want to pay for coverage you won’t eventually need. A single $1.5 million, 30-year term policy provides a flat death benefit. You pay the same premium in year 29 as you did in year one. While this is simple, it creates the problem of “wasted premium.” By the time you reach the final decade of that policy, your mortgage is likely smaller and your children are probably financially independent. You’re effectively paying for a massive amount of coverage that no longer matches your actual financial risk.

The Literal Dollar Savings

The math behind life insurance laddering is compelling. For example, a healthy 35-year-old male might pay $1,450 annually for a single $1.5 million, 30-year term policy. Over the life of the plan, the total cost reaches $43,500. If we split that coverage into three $500,000 policies with 10, 20, and 30-year terms, the initial combined premium might start near $900. As the shorter rungs expire, the total annual cost drops significantly.

- Years 1-10: $900 per year

- Years 11-20: $600 per year

- Years 21-30: $350 per year

In this scenario, the total cost over 30 years is approximately $18,500. That is a savings of $25,000, or roughly 57% compared to the single policy. We help visitors run these specific numbers using our proprietary tools to find the exact configuration that fits their budget. These saved premiums don’t just sit idle; you can redirect them into retirement accounts or college funds where they can grow for decades.

Flexibility and Control for the Prospect

A laddered approach empowers prospects to be their own financial architects. Life is unpredictable. If you receive an unexpected inheritance or pay off your mortgage ten years early, you can simply “drop a rung” by canceling one of the individual policies. A single large policy is an all-or-nothing commitment. If you want to reduce your coverage on a single policy, you often have to go through a complicated reduction process or cancel the whole thing and re-apply at an older, more expensive age.

We believe in making this process transparent. You can get term life insurance quotes on our website right now without sharing your name, phone number, or email address. This allows you to test different laddering combinations privately. If you’re looking for other products like whole life or disability insurance, we require contact information up front. This is because we need to have a discussion with a prospect before quoting those complex products to ensure the coverage is accurate.

The only real trade-off is administrative. You’ll manage three bills instead of one. For most visitors, the minor inconvenience of tracking three digital invoices is a small price to pay for keeping thousands of dollars in their own pockets.

Step-by-Step: How to Calculate Your Personal Ladder Rungs

Building a life insurance laddering strategy requires a clear view of your financial future. We recommend a methodical approach to ensure your family remains protected while you minimize unnecessary premium costs. Follow these four steps to define your rungs.

- Step 1: Itemize your debts. List every major financial obligation, including your mortgage, car loans, and private student loans. Note the exact number of years remaining on each balance.

- Step 2: Calculate income replacement. Determine how many years of your annual salary your family would need to maintain their standard of living. Usually, this is highest while children are young.

- Step 3: Map your timeline. Align your totals onto a 10, 20, and 30-year horizon. You will likely see your total need drop significantly at each decade mark.

- Step 4: Identify the floor. This is the permanent base of coverage you want to keep for life, often used for final expenses or legacy planning.

Identifying Your Declining Liabilities

Your “debt load” changes as you age. To get an accurate figure, we suggest using this checklist: mortgage balance, total credit card debt, and anticipated education costs. If you have children entering university around 2026, factor in a 4% annual inflation rate for tuition based on recent historical averages. This ensures your life insurance laddering plan doesn’t fall short. Also, account for Social Security survivor benefits. These payments can act as an offset in your later rungs, allowing you to reduce private coverage as you approach retirement age.

Determining the Right Coverage Mix

Most visitors find that the top rungs of their ladder, which cover temporary needs like a 20-year mortgage, are best served by term policies. You can see term life insurance quotes on our site instantly. We value your privacy, so you can view these rates without providing your name, email, or phone number. We want you to feel empowered to research at your own pace.

The bottom rung of your ladder is different. This “floor” usually consists of permanent coverage that lasts your entire life. If you are interested in this, you can submit a permanent life insurance quote request. For these products, we require your contact information up front. This is because permanent policies are complex. We need to have a detailed discussion with prospects to ensure the policy is tailored to your specific estate goals before providing a quote. We are here to guide you through those permanent components whenever you are ready.

Ready to see how affordable your customized protection can be? Compare instant term quotes now without sharing your personal data.

Implementing Your Strategy with LifeInsure.com

Building a life insurance laddering strategy shouldn’t feel like a high-pressure sales pitch. We designed our platform to be a transparent resource for visitors who want to take control of their financial future. Our “Privacy First” approach sets us apart from typical insurance sites. We believe you should have the space to model your coverage without immediate solicitation. You can explore different policy lengths and amounts at your own pace, ensuring the final structure matches your specific life stages.

Instant Quotes for Your Term Rungs

The foundation of most ladders consists of multiple term policies. You can get term life insurance quotes on our site without entering your name, phone number, or email address. This allows for risk-free modeling of your entire ladder. You might want to see how a $1 million 30 year policy compares to a combination of shorter terms. By trying different combinations of years and coverage amounts, you can find the exact price point that fits your monthly budget. It’s a fast, easy way to see how life insurance laddering reduces your long-term costs by thousands of dollars.

Expert Guidance for Complex Needs

While term life is simple to quote anonymously, other financial tools require a more personalized touch. For products like whole life, disability insurance quotes, or long-term care, we require your contact information up front. We need to have a discussion with a prospect before quoting them these specific products. These policies have moving parts that require expert calibration to function correctly within a ladder. We want to make sure your “permanent” base or your income protection is structured to provide the maximum benefit without wasted premium dollars.

When you provide your information for these complex needs, you aren’t just a number in a database. You’ll work directly with an experienced independent agent who stays with you from start to finish. We don’t use the impersonal call center model. Your agent acts as an educator and advocate, helping you make an educated decision based on your unique health profile and financial goals. We’ve helped over 100,000 families secure their futures, and we apply that experience to every ladder we build.

We take your trust seriously. Don’t worry about your personal data; we never sell or share your info with third parties. Our process is built on these core values:

- Honesty: We provide clear, direct answers about policy costs and requirements.

- Security: Your data is protected by industry-leading encryption and privacy standards.

- Independence: We represent many top-rated carriers, not just one, to ensure you get the best rate.

- Accessibility: Have questions? You can call us and speak to a real person immediately.

Finalizing your ladder is the last step toward total peace of mind. Whether you’re just starting to model your term rungs or you’re ready to integrate disability protection, we’re here to guide you. Use our quote engine to start your journey, or reach out to our team to refine your strategy. We’re ready to help you build a plan that’s as unique as your life.

Take Control of Your Financial Future Today

Implementing life insurance laddering is a smart way to ensure your family stays protected without overpaying for unnecessary coverage. By matching specific policy terms to your 25 year mortgage or your children’s 4 year college tuition, you create a flexible safety net that evolves with you. This strategy can reduce your total premium costs by 15% or more compared to maintaining one large policy for 30 years.

We make the planning process transparent and stress-free. You can instantly compare rates from 40+ top-rated carriers through our online engine. If you want term life insurance quotes, we don’t require any personal information like your name or phone number. For specialized products like whole life or disability insurance, we ask for contact details up front. We do this because we need to have a discussion with a prospect before quoting them to provide an accurate assessment. You’ll work directly with an experienced independent agent who guides you personally, as we never use impersonal call centers.

Get Your Instant, Anonymous Term Life Quote and Build Your Ladder Today

Now it’s time to secure your peace of mind with a plan that fits your life.

Frequently Asked Questions

Is it better to have one large life insurance policy or several smaller ones?

Having several smaller policies is often more cost-effective because your total coverage decreases as your financial obligations drop over time. If you buy three separate term policies instead of one massive 30-year plan, you could save 20% or more on total premiums. We make it easy to see these savings; you can get term life insurance quotes on our site instantly without sharing your name, phone number, or email address.

Does laddering life insurance cost more in administrative fees?

You’ll pay a separate policy fee for each individual rung, but the total premium savings usually far exceed these small costs. Most insurance companies charge an annual administrative fee between $65 and $90 per policy. Even with three separate fees, life insurance laddering typically costs less than maintaining a single, high-limit policy for decades after your mortgage is paid off.

Can I add a new rung to my ladder later in life?

You can certainly add a new policy to your ladder whenever your financial responsibilities grow unexpectedly. If you start a new business at age 45, you might add a 10-year term policy to cover that specific debt. You don’t need to provide any personal information to see instant term quotes for these new rungs on our platform, which helps you stay in control of your budget.

What happens if I pay off my mortgage early in a laddering strategy?

You can simply cancel the specific policy that was tied to that debt once the mortgage balance reaches zero. If you pay off your home 7 years early, you stop paying those premiums immediately and keep your other rungs active for your remaining needs. This flexibility is why we recommend this strategy for homeowners who plan to be aggressive with their debt payments over the next 15 to 20 years.

Can I use different insurance companies for different rungs of my ladder?

Using different insurance companies is a smart way to diversify your coverage and find the lowest rates for each specific term length. One carrier might have the best price for a 10-year term while another leads the market for 20-year plans. We work with 40 plus top-rated carriers to help you compare and find the best fit for every stage of your life.

Is laddering life insurance only for wealthy individuals?

No, life insurance laddering is a practical tool for middle-class families who want to maximize their monthly cash flow. A 35-year-old parent can often reduce their monthly insurance bill by $25 or more by using multiple shorter terms rather than one expensive long-term policy. It’s about being smart with your budget and only paying for the protection your family actually needs today.

How do I manage the expiration dates of multiple policies effectively?

We suggest setting digital alerts and reviewing your coverage during your annual tax preparation or financial checkup. Keeping a simple spreadsheet with your three or four policy numbers and their expiration dates ensures you aren’t caught off guard. Our experienced agents stay with you from start to finish to help you track these milestones and adjust your coverage as your life changes.

Can I ladder permanent life insurance with term life insurance?

You can absolutely combine permanent and term insurance to create a lifetime safety net. While you can get term quotes anonymously on our site, we require your contact information up front for whole life, disability, or long-term care quotes. We need to have a discussion with you before quoting these products to ensure the complex features and riders are tailored correctly to your specific financial situation.