By Richard Reich | Independent Life Insurance Broker | CA License #0832938 | 30+ years specializing in impaired risk and high-risk life insurance placements.

When term life insurance expires, the coverage ends and the insurance company no longer pays a death benefit if the insured person passes away. In most cases, you can either let the policy expire, renew it at a higher premium, convert it to permanent life insurance if your policy allows, or apply for a new term policy. The best option depends on your age, health, budget, and whether your loved ones still need financial protection.

What if the end of your 20-year term policy wasn’t a financial crisis, but actually the best time to lock in a better rate for your future? Most prospects feel a genuine sense of dread when they see that final expiration date approaching. You might worry about premium increases that can jump by 800% overnight or fear that a health change since your last exam makes you uninsurable. It’s completely normal to feel overwhelmed when figuring out what happens when term life insurance expires, especially when you’re trying to tell the difference between a policy reaching its end and accidentally letting it lapse.

We’re here to help you manage these choices with confidence. You’ll learn exactly how to secure new coverage without overpaying or getting stuck with automatic renewal rates that drain your bank account. This guide provides a clear roadmap for comparing new rates, understanding conversion riders, and protecting your family’s legacy. At LifeInsure.com, we prioritize your privacy. Visitors can compare term life quotes right now without entering a name, phone number, or email address. For other products, such as whole life or disability insurance, we require contact information up front. We believe it’s vital to have a discussion with a prospect before quoting those specific plans to ensure the coverage is a perfect fit.

Key Takeaways

Understand the critical shift from level premiums to costly annually renewable rates to avoid a sudden lapse in your family’s protection.

Learn exactly what happens when term life insurance expires and how to evaluate your primary options for maintaining or ending coverage.

Use our 2026 audit checklist to review your current debts and your loved ones’ financial dependence before your policy reaches its end date.

We allow visitors to access term life quotes without entering personal information, though for other coverage like whole life or disability, we require contact info up front so we can have a discussion with a prospect before quoting them.

Discover how our independent agents provide a personalized, “privacy first” experience that helps you navigate policy expiration without the pressure of a call center.

Table of Contents

What Happens When Your Term Life Insurance Reaches Its Expiration Date?

How We Help You Navigate Policy Expiration at LifeInsure.com

What Happens When Your Term Life Insurance Reaches Its Expiration Date?

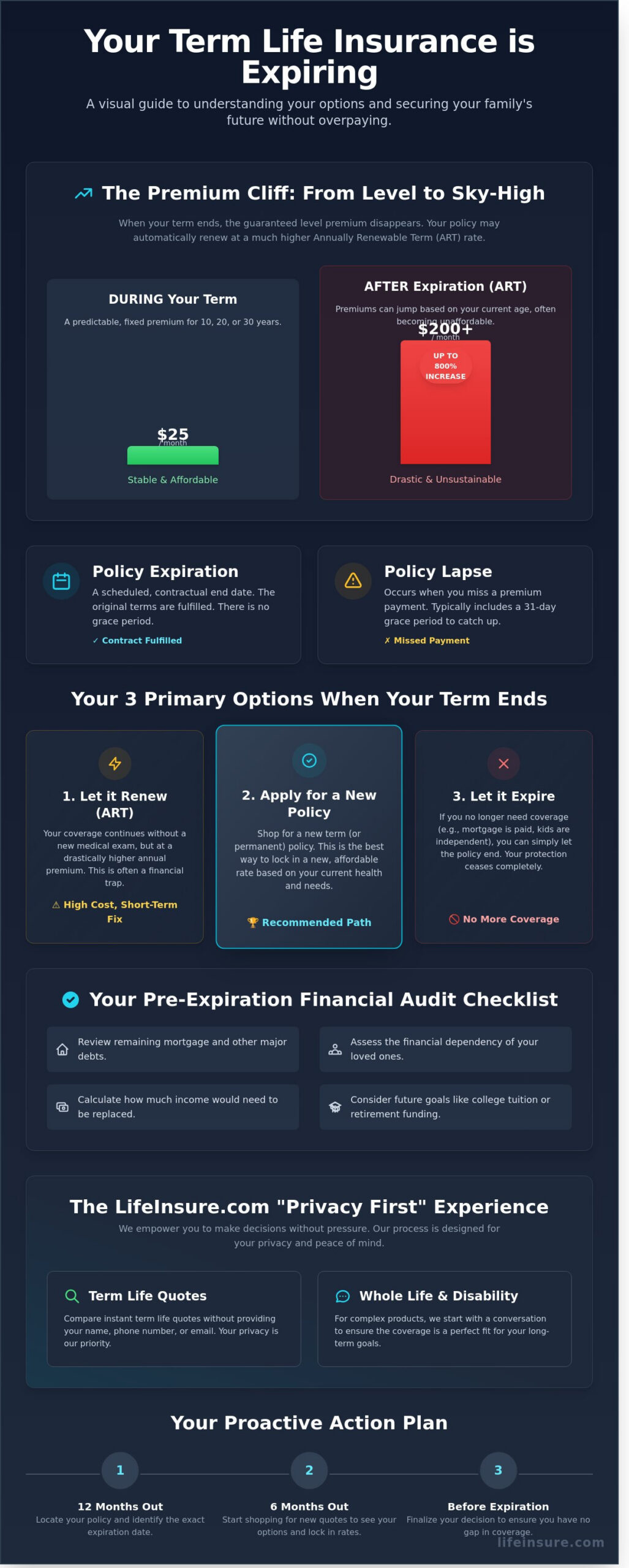

Reaching the final day of a 10, 20, or 30-year term is a significant milestone for your financial planning. It means you’ve successfully protected your family during periods of high financial vulnerability, such as the years of a primary mortgage or while raising children. However, understanding what happens when term life insurance expires is vital for maintaining your peace of mind. On the exact date specified in your policy contract, the initial level period ends. This shift changes your coverage from a fixed-cost asset into a much more expensive, short-term arrangement.

The most immediate change is that the death benefit protection effectively ceases to exist under the original terms. If a policyholder passes away even one day after the expiration date, beneficiaries are no longer eligible for a payout. This is why we encourage visitors to review their documents at least 12 months before the term ends. At LifeInsure.com, we believe in making this transition stress-free. If you are looking for new coverage, you can use our tool to get Term life insurance quotes instantly without providing your name, phone number, or email address. We value your privacy and want you to feel empowered during your search.

For other products like whole life, disability insurance, or long-term care, we require contact information up front. We take this approach because these products are complex; we need to have a discussion with a prospect before quoting them to ensure the coverage matches their specific health profile and long-term financial goals. Whether you need a simple term policy or a more permanent solution, our goal is to act as your experienced guide.

The End of Level Premiums

During your initial term, you enjoyed a level premium. This is the fixed monthly or annual cost you agreed to when you first signed your contract. This price is guaranteed not to change for the duration of the term, whether that was 10 or 30 years. When the term expires, that price guarantee officially disappears. While coverage doesn’t always stop immediately, the cost structure shifts to an annually renewable rate. This means your premium will jump significantly based on your current age. For example, a 30-year-old paying $25 a month might see that cost spike to $200 or $400 a month once they hit age 60 and the term ends.

The Grace Period vs. Expiration

It’s easy to confuse a policy expiration with a policy lapse, but they are different events. A lapse occurs when you miss a premium payment, usually triggering a standard 31-day grace period to get caught up before the insurance company cancels the policy. In contrast, expiration is a scheduled contractual event. There is no grace period for an expiring term. Once that date passes, the original contract is fulfilled. We advise all prospects to locate their original policy documents and highlight the “Expiry Date” or “Term End Date.” Knowing what happens when term life insurance expires in advance allows you to shop for a new policy while you are still covered, ensuring there is never a day when your family is left unprotected.

Death Benefit: Ends at 11:59 PM on the final day of the term.

Premium Costs: Shift from level to annually renewable, often increasing by 500% or more.

Eligibility: Payouts are only valid if the death occurs within the active term dates.

Action Plan: Start shopping for new quotes at least six months before expiration to lock in lower rates based on your current health.

We are here to help you navigate these choices without the pressure of a high-volume call center. You’ll work with an experienced independent agent who stays with you from start to finish. Our process is fast, easy, and designed to give you the honest answers you need to protect your family’s future.

Understanding the Automatic Renewal Clause and Price Hikes

Most visitors are surprised to find that their $50 monthly premium can suddenly jump to $450 or even $1,000 overnight. This happens because almost every policy includes an Annually Renewable Term (ART) provision. While this clause sounds helpful, it is often a financial trap. It allows you to keep your coverage without a new medical exam, but the insurance company charges a much higher premium to offset the increased risk. We often see rates increase by 500% to 2,000% in the very first year after the initial term ends. If you are wondering what happens when term life insurance expires, the short answer is that you stay covered, but the cost becomes prohibitive for most families.

We want you to understand that these price hikes aren’t random. They are calculated based on the fact that you are older and potentially less healthy than you were 20 years ago. While we provide instant term life insurance quotes without requiring your name or phone number, other products like whole life or disability insurance require contact info up front. This is because we need to have a discussion with a prospect before quoting those complex products to ensure the numbers are accurate for your specific situation.

Why Premiums Skyrocket After the Term

The primary reason for these extreme price hikes is a concept called adverse selection. Insurance companies realize that healthy prospects will simply shop for a new policy at market rates. Therefore, the insurer assumes that the only people choosing to pay the high renewal rates are those who are too ill to qualify for coverage elsewhere. To protect their bottom line, they price the ART premiums as if every policyholder in that pool has a serious health condition. An annually renewable term is a mechanism that maintains your coverage at your current age-based risk level without requiring new evidence of insurability. This creates a safety net for the unhealthiest individuals, but it makes the cost unsustainable for everyone else.

The Role of Annually Renewable Term (ART)

When you look at Term Life Insurance Policies from major carriers, you will see that ART premiums are not level. They increase every single year as you age. A premium that feels expensive at age 55 will become mathematically impossible by age 65. We have seen cases where a policyholder pays $2,500 in year 21 of a 20-year term, only to see that bill climb to $3,800 in year 22. This is why ART is rarely a sustainable long-term financial strategy for our prospects.

You should view the ART provision only as a very short-term bridge solution. It’s useful if you are 30 days away from closing a large loan or in the middle of medical treatment that prevents you from applying for a new policy immediately. However, staying on an ART schedule for more than a few months will quickly drain your savings. If you want to know what happens when term life insurance expires in a practical sense, it means your “affordable” period has ended, and a much more expensive phase has begun. We recommend evaluating your options at least 12 months before your current term expires to avoid these automatic price hikes.

Managing such a sudden, significant expense can be challenging. For individuals who need to cover immediate costs while securing a more affordable long-term policy, resources like QuickCashDirect offer short-term financial solutions.

Your Three Primary Options After a Policy Expires

When you reach the end of your level premium period, you face a critical decision point. Understanding what happens when term life insurance expires is the first step toward securing your 2026 financial goals. We see visitors choose one of three distinct paths based on their current health, debt levels, and family needs. Each path carries different costs and long-term implications for your estate. We want to help you weigh these choices by looking at your current age and liabilities. If you are 55 and still have 10 years left on a mortgage, a new 10-year term might be perfect. If you have developed a chronic condition, conversion is likely the smarter move.

The first option is simply letting the policy lapse. This makes sense if your original financial obligations no longer exist. Perhaps you bought a 20-year term in 2004 to cover a mortgage that is now paid off. If your children are financially independent and your retirement accounts are fully funded, you might not need to pay for coverage anymore. We recommend reviewing your 2026 budget to see if those premium dollars are better spent on long-term care insurance or supplemental retirement savings. If your death would not cause a financial hardship for anyone, allowing the policy to expire is a valid and cost-effective choice.

The second and third options involve maintaining coverage through different methods. You can either transition your existing policy into a permanent one or start over with a fresh application. Both choices have pros and cons depending on your physical health and how much you want to pay each month. We focus on providing clarity so you don’t feel overwhelmed by the technical jargon often found in insurance contracts. Knowing what happens when term life insurance expires helps you avoid the “automatic renewal” trap, where premiums can jump by 500 percent or more in a single month.

Converting to a Permanent Life Insurance Policy

Many policies include a conversion privilege. This feature lets you switch to a permanent plan without taking a new medical exam. This is a lifesaver if your health has declined since you first applied. Because these products are complex and involve cash value components, we require contact information up front for permanent life insurance quotes. We need to have a discussion with a prospect before quoting permanent products. This ensures the policy structure matches your specific goals, such as estate liquidity or legacy planning. These plans are more expensive than term, but they provide coverage for your entire life.

Applying for a New Term Life Policy

If you are still in good health, starting a new term is usually the most affordable way to maintain a safety net. You can view instant term life insurance quotes on our site right now. Unlike other sites, we don’t ask for your name, phone number, or email just to see prices. A new policy requires full underwriting. This process often includes a health questionnaire and a brief medical exam to check your blood pressure and cholesterol. If you have maintained a healthy lifestyle, you can often secure a new 10 or 20-year term at a rate that fits comfortably within your monthly expenses.

Option 1: Let the policy end if your mortgage is paid and your kids are grown.

Option 2: Use the conversion privilege if you have health issues and need lifelong coverage.

Option 3: Apply for a new term if you are healthy and want the lowest possible premium.

We believe in empowering you to make an educated decision. Our goal is to provide the tools you need to compare these paths side by side. Whether you want to browse quotes anonymously or speak with an experienced independent agent, we are here to guide you through the transition. Taking action before your current policy officially ends ensures there are no gaps in your family’s protection.

How to Decide If You Still Need Life Insurance in 2026

Deciding your next step requires a clear-eyed look at your 2026 balance sheet. Many visitors worry about what happens when term life insurance expires, but the reality is often simpler than you think. Your needs have likely shifted since you first signed that 20-year contract back in 2006. We believe in empowering you with data so you can make an educated choice without the pressure of a call center environment.

Start by auditing your current debt. If your mortgage was $350,000 a decade ago but is now $42,000, your need for a massive death benefit has dropped. We suggest totaling your remaining personal loans, credit card balances, and any outstanding private student loans. If these totals are under $100,000, a smaller, more affordable policy might be the smartest move for your budget. You don’t always need to replace the full value of your original policy to keep your family secure.

Assessing Your Current Financial Obligations

Ask yourself if your children are now financially independent. If they graduated from college in 2024 or 2025 and have started their own careers, the “income replacement” math changes. You’re no longer covering 20 years of future tuition and housing. Instead, you might only need to protect your spouse’s retirement lifestyle. We often see prospects transition from a $1 million policy to a $250,000 policy because their primary obligations have been met. This shift can save you hundreds of dollars in annual premiums while still providing a necessary safety net.

Don’t forget to consider “Final Expense” needs. The average cost of a funeral and burial in 2024 reached approximately $8,300, according to the National Funeral Directors Association. If you have significant savings, you might self-insure for these costs. If not, a small permanent policy or a short-term 10-year policy can ensure these expenses don’t fall on your grieving relatives.

If this type of dedicated coverage sounds right for you, you can learn more about The Paul Group, an agency that specializes in these plans for seniors.

Evaluating Your Health and Insurability

Your health is the biggest factor in determining your 2026 rates. Age-related changes are inevitable. If your blood pressure has climbed above 140/90 or your cholesterol levels have shifted in the last 18 months, new term rates will reflect that. However, even with these changes, we can often find competitive options through our network of independent carriers. We focus on finding the right fit for your specific health profile rather than a one-size-fits-all approach.

We want to be transparent about how we provide quotes. If you want a term life insurance quote, you can get one on our site instantly without entering your name, phone number, or email address. We value your privacy. However, for specialized products such as disability insurance, we require you to provide your contact information up front. This is because these products are complex. We need to have a direct discussion with you before providing a quote to ensure the coverage meets your occupational needs. If you have specific health concerns, such as a recent diabetes diagnosis or a heart condition, that might complicate a new application, please contact us directly. We prefer to work as your advocate to navigate these challenges together.

Understanding what happens when term life insurance expires is the first step toward a secure future. Whether you need a full replacement or a smaller “Final Expense” policy, we are here to guide you through the transition.

Compare your 2026 term life options today

How We Help You Navigate Policy Expiration at LifeInsure.com

We’ve spent over 25 years helping families secure their futures. Our team functions as independent brokers rather than a high-pressure call center. This distinction matters for your wallet. Captive agents can only sell you one brand. We compare dozens of A-rated carriers to find the best fit for you. Our priority is a smooth transition, as even a single day without coverage puts your beneficiaries at risk. Our process ensures you understand exactly what happens when term life insurance expires, so you aren’t surprised by a sudden loss of benefits.

Most people don’t realize that a typical application process lasts between 4 and 8 weeks. If you wait until your current policy ends to start looking, you’ll likely face a coverage gap. We manage this timeline for you. We coordinate the medical exams and gather the necessary physician statements. We aim to have your new policy active before your old one ends. This proactive approach saves you from the “guaranteed renewal” trap, where premiums can jump from $50 a month to $500 a month overnight. We provide the clarity you need to move forward with confidence.

Get Instant Term Quotes Without Sharing Personal Data

You shouldn’t have to give up your privacy just to see a price. Our term quote engine is built on a “Privacy First” philosophy. You can view 2026 rates from top carriers without entering your name, phone number, or email address. This allows you to shop freely without fear of sales pressure or endless follow-up calls. Use our tool to benchmark your current carrier’s renewal offer. Many renewal offers are 2 to 3 times more expensive than a new policy. Checking the market first ensures you don’t overpay for the next phase of your life.

Transparency is the foundation of our service. By providing these instant quotes, we empower you to make an educated decision on your own terms. You can compare the costs of a 10, 15, or 20-year term in seconds. This data helps you prepare for what happens when term life insurance expires by securing a new policy at a rate that fits your current budget. We believe in providing value before we ever ask for your contact details.

Specialized Guidance for Permanent and Disability Coverage

Some insurance products are too complex for a simple online calculator. For whole life, disability, or long-term care insurance, we require your contact information up front. We need to have a detailed discussion with you before providing a quote for these specialized products. Accuracy depends on understanding your specific health history and financial goals. These policies often involve complex riders that can significantly change the premium and the value of the coverage.

Our team stays with you from the initial quote through the final policy delivery. We take the time to explain the requirements for different types of insurance so there are no surprises during underwriting. Whether you are looking for a policy that builds cash value or one that protects your income in the event of disability, we provide expert consultation. We act as your advocate, ensuring the insurance company sees the full picture of your health and lifestyle. This personalized support is why our clients trust us to handle their most important financial protections.

Secure Your Family’s Financial Future for 2026

Your current policy won’t last forever, but your peace of mind should. Understanding what happens when term life insurance expires helps you avoid the 800% to 1,500% price hikes often found in automatic renewal clauses. Since 2005, we’ve helped visitors compare top-rated carriers to find the most affordable rates available. We aren’t a call center. You’ll work with an experienced independent agent who guides you through every step of the process.

If you’re shopping for term life, you can see rates instantly. We don’t require your name, phone number, or email for these specific quotes. For other products, such as whole life, disability, or long-term care, we require contact information up front. We need to have a discussion with a prospect before quoting those complex plans to ensure accuracy. Don’t let your coverage gap. It’s easier than you think to stay protected and confident in your choice.

Compare Instant Term Life Quotes Anonymously

Frequently Asked Questions

Can I renew my term life insurance after it expires?

Yes, most policies allow for guaranteed renewal on an annual basis. We warn visitors that the premiums will be significantly higher than the original level rate. Because the insurer no longer has the protection of a fixed 10 or 20-year contract, your costs could jump by 800% or more in the first year alone. This option is best for those who only need a few extra months of coverage.

What is the difference between a policy expiring and lapsing?

Expiration is the natural end of the contract term, such as the final day of a 20-year agreement. A lapse occurs when you stop paying premiums before that term ends. While an expired policy has no remaining value, a lapsed policy can sometimes be reinstated if you pay the overdue balance within 31 days. Understanding what happens when term life insurance expires helps you avoid these unexpected coverage gaps.

Do I get any money back when my term life insurance expires?

No, standard term life insurance does not have a cash value component. It’s pure insurance protection that pays a benefit only if the insured person dies during the 10-, 20-, or 30-year term. If you don’t die during the term, the insurance company keeps the premiums, and the coverage ends. You won’t receive a refund of the $40 or $80 you paid monthly unless you purchased a specific return-of-premium rider.

Is it better to convert my policy or buy a new one?

Buying a new policy is 30% to 50% cheaper if you’re still in good health. However, if you’ve developed a chronic condition since your 2015 policy started, converting to a permanent policy is better. Conversion doesn’t require a new medical exam, though premiums will be higher than term rates. While we provide anonymous term quotes, we require contact info up front for whole life or disability products because we must discuss the products with a prospect before quoting them.

How long before my policy expires should I start looking for new coverage?

We recommend that prospects start comparing rates at least 3 to 6 months before the expiration date. This 180-day window provides ample time for the underwriting process, which can take 4 to 8 weeks to complete. You can get instant term quotes on our site without entering your name, phone number, or email. For other products like long-term care, we require contact info up front so we can have a discussion with you first.

What happens if I die the day after my term insurance expires?

If the policy has officially expired and you haven’t exercised a renewal or conversion option, there is no coverage. The insurance company is not legally obligated to pay the $500,000 or $1,000,000 death benefit to your beneficiaries. This is why we emphasize planning ahead and knowing exactly what happens when term life insurance expires. A single day of being uninsured can leave your family without the financial safety net you intended to provide.

Last Updated on June 12, 2026 by Sonny O'Steen