What if you could participate in stock market gains without the risk of losing a single penny of your initial investment? It sounds like a dream, yet 60% of retirees in a 2024 survey listed outliving their money as their top fear. An indexed annuity offers a unique middle ground. It’s built to capture a portion of market growth while keeping your principal locked away from volatility. We understand that the insurance industry often hides behind complex jargon and 10% surrender charges. That’s why we’re here to simplify things.

We believe you deserve a retirement strategy that feels secure and transparent. In this guide, we’ll explain how indexed growth works and help you decide if it’s a safer alternative to direct investing. While we offer instant term life quotes without asking for your name, products like an indexed annuity require a different approach. Because these plans are complex, we need to have a discussion with prospects before providing a quote. We’ll ask for your contact information up front so we can provide the honest, personalized guidance you need to make an educated decision for 2026 and beyond.

Key Takeaways

-

Learn how to shield your principal from market volatility while still capturing growth potential tied to major indices such as the S&P 500.

-

Understand the specific mechanics, such as caps and participation rates, that insurance companies use to balance your growth with downside protection.

-

Compare the "safe but slow" nature of fixed contracts against the growth potential of an indexed annuity to see which strategy fits your 2026 goals.

-

Discover the truth about surrender charge schedules and how to structure your contract to maintain financial flexibility over time.

-

Understand why we require contact information up front for these products: we believe a direct discussion with prospects is essential to choosing the right plan.

Table of Contents

-

What Is an Indexed Annuity and How Does It Protect Your Future?

-

Understanding the Mechanics: Caps, Participation Rates, and Spreads

-

Indexed vs. Fixed vs. Variable: Which Is Better for Your Goals?

-

Practical Considerations: Surrender Charges and Payout Options

What Is an Indexed Annuity and How Does It Protect Your Future?

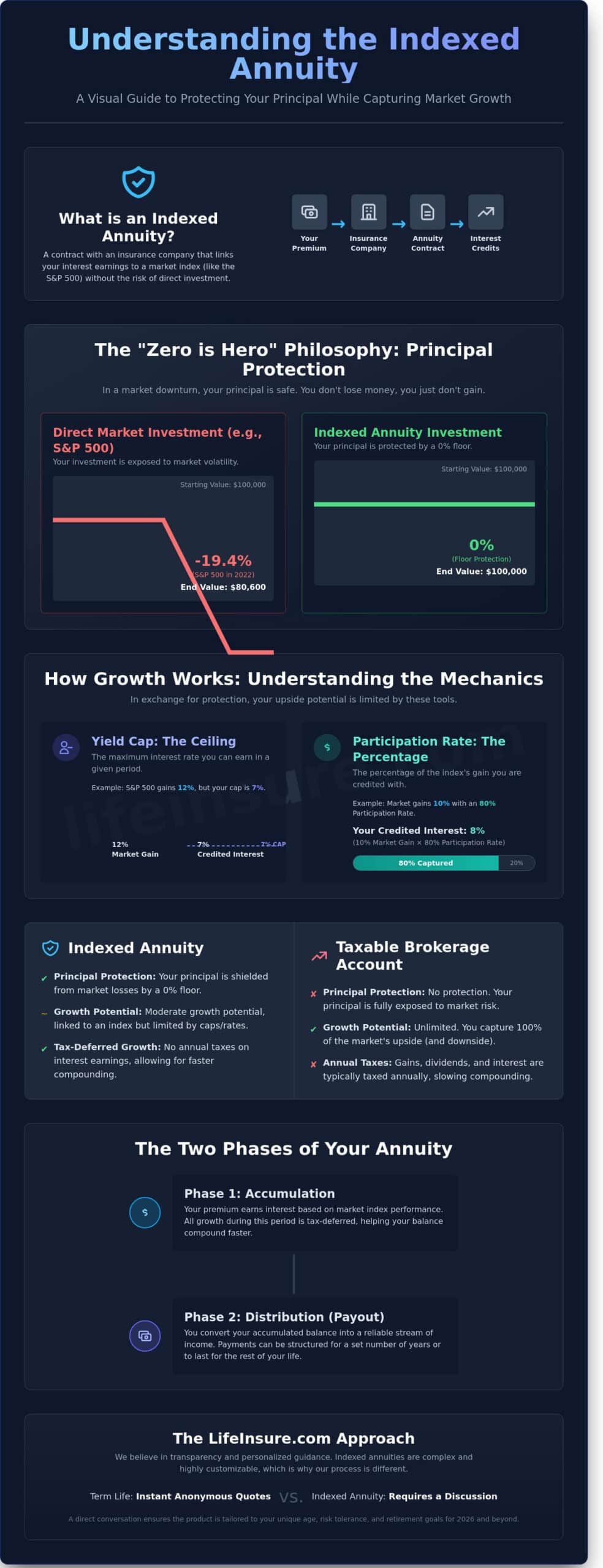

An indexed annuity is a formal contract between a visitor and an insurance company. You provide a lump sum or a series of payments, and in exchange, the insurer promises to credit your account with interest based on the performance of a specific market index. We classify these products as fixed indexed annuities (FIAs). They’re distinct from variable annuities because they don’t involve direct investment in the stock market. Instead, they offer a middle ground between the safety of a traditional fixed annuity and the growth potential of an equity fund. For a foundational look at how these contracts evolved, you might find Wikipedia’s guide to equity-indexed annuities helpful for understanding the underlying mechanics.

At LifeInsure.com, we believe in transparency regarding the quoting process. While visitors can get instant term life quotes on our site without sharing a name or email, annuities require a different approach. We require contact information up front for an indexed annuity. We need to have a discussion with a prospect before quoting them because these products are highly customizable. Factors like your age, retirement timeline, and risk tolerance change, which carrier or contract will serve you best? We take the time to ensure the strategy aligns with your goals before providing specific numbers.

Every contract moves through two primary stages. The accumulation phase is the period where your principal earns interest based on market movements. Later, you enter the distribution or payout phase. This is when the insurance company converts your balance into a stream of income. You can choose to receive these payments for a set number of years or as a guaranteed paycheck that lasts for the rest of your life. This structure provides a predictable path from saving to spending during your retirement years.

The ‘Zero is Hero’ Philosophy

This strategy focuses on principal protection. During the 2022 market downturn, the S&P 500 lost 19.4% of its value. Prospects with an indexed annuity didn’t lose a penny of their principal because of the protective floor. This appeals to visitors who remember the 37% drop in 2008 and want to avoid similar losses. The floor is the minimum guaranteed interest rate, usually 0%.

Tax-Deferred Growth Explained

Interest earnings aren’t taxed until a visitor makes a withdrawal. In a taxable brokerage account, a 24% or 32% tax rate can significantly slow down your progress every year. Annuities let you skip the annual tax bill, which helps your balance compound much faster over time. This makes them an excellent tool for late-stage retirement planning for those aged 50 to 65. You keep more funds working for your future.

We’re here to help you make an educated decision. If you have questions about how these phases work or why we require a conversation before providing a quote, give us a call. We stay with you from start to finish to ensure you feel secure in your choice.

Understanding the Mechanics: Caps, Participation Rates, and Spreads

Insurance companies use specific financial tools to provide the "floor" that protects your principal. These tools, often called levers, allow them to manage the risk of market volatility. It’s a trade-off. You get protection from losses, but you don’t get 100% of the market’s upside. You also don’t own any stocks or bonds within the index itself. Instead, the insurance company uses your premium to buy fixed-income assets and options. This structure ensures your account value won’t drop if the index falls by 19.4% in a single year, which is exactly what the S&P 500 did in 2022. Understanding how these levers work is the only way to calculate the potential return on an indexed annuity.

We believe in transparency. These mechanics can feel overwhelming at first, but they’re just math equations the company uses to balance its risk. We help prospects decipher these terms during our initial discussion. Unlike term life insurance, where you can see instant quotes anonymously, these products require a deeper look at the specific contract language. These levers can change over time, so you need to know what you’re signing before you commit your retirement savings.

Yield Caps and Participation Rates

A "Cap" is the ceiling on your interest earnings. If the S&P 500 grows by 12% in a year but your contract has a 7% cap, your account is credited with 7%. The insurance company keeps the excess to fund your downside protection. A "Participation Rate" works differently. It’s the percentage of the index’s gain that we credit to your account. For example, if the index grows 10.5% and your participation rate is 80%, you earn 8.4% interest. Some contracts offer a 100% participation rate but include a cap. Others might have no cap but a lower participation rate. We help you compare these options to see which fits your risk tolerance.

Spreads and Asset Fees

The "Spread" or margin is a flat percentage deducted from the index’s total gain. If the index increases by 10% and your contract has a 3% spread, your net gain is 7%. These are implicit costs. They differ from the explicit fees found in variable annuities, which can often range from 2.5% to 4% annually regardless of performance. Many visitors prefer "no-fee" contracts in which the insurance company earns its margin solely from the spread. This means if the market is flat, you aren’t losing money to administrative fees. It’s a cleaner way to protect your balance while still participating in market growth.

Because every indexed annuity has different combinations of these levers, we don’t provide instant online quotes for them. While you can get term life quotes on our site without entering your name or email, we require contact information up front for annuity products. We need to have a detailed discussion with you first. This ensures we match you with a contract that actually meets your income needs. You’ll work directly with an experienced independent agent who will walk you through the fine print of spreads and caps before you make any decisions.

Indexed vs. Fixed vs. Variable: Which Is Better for Your Goals?

Choosing a retirement vehicle in 2026 requires a clear understanding of how risk affects your long-term security. We categorize these options into three distinct buckets to help visitors find their ideal fit. Each product serves a specific purpose, whether you prioritize absolute safety or higher growth potential. Your choice will dictate how your principal behaves when the market fluctuates. We focus on products that provide a predictable foundation for your future rather than those that leave your savings vulnerable to sudden economic shifts.

Fixed Annuities: The Conservative Baseline

Fixed annuities function much like a long-term certificate of deposit issued by an insurance company. They offer a guaranteed interest rate for a set period, such as 4.85% for a five-year term. We find that prospects choose this option when they have zero tolerance for market volatility. If you want to know exactly how much your account will be worth on a specific date, this is the right path. We can provide these quotes after we have a brief introductory call to discuss your liquidity needs.

Variable Annuities: High Risk, High Reward

Variable annuities involve direct investment in the stock market through sub-accounts. This means your principal can lose value. If the S&P 500 drops 15%, your account balance could reflect that loss. Because of this exposure, these are considered securities and require specific regulatory oversight. We generally steer visitors toward "safety first" products. We believe most prospects want to avoid the anxiety of watching their retirement nest egg shrink during a market correction.

The indexed annuity serves as the middle ground between these two extremes. It provides a 0% floor, ensuring you never lose money during market downturns. In exchange for this protection, your gains are typically capped. For instance, if the market surges 12%, your indexed annuity might be capped at 9.5%. This balance allows you to outperform standard fixed rates while maintaining the peace of mind that your principal is secure. It is a permanent product designed for those who want growth without the "downside" risk of variable accounts.

We handle the quoting process for these products differently than we do for term life insurance. While visitors can get term life quotes on our site without entering a name or phone number, annuities require your contact information up front. This is because these products are complex. We need to have a discussion with a prospect before quoting them to ensure the contract terms align with their specific financial goals. Our experienced independent agents work with you from start to finish to clearly explain these details.

-

Fixed: Best for those who want a simple, guaranteed interest rate.

-

Indexed: Best for those seeking market-linked growth with a 0% loss floor.

-

Variable: Best for those comfortable with losing principal in exchange for unlimited growth.

Your long-term financial security depends on matching the right product to your personal risk profile. We prioritize education because an informed visitor makes better decisions. By choosing an indexed or fixed product, you eliminate the fear of outliving your money due to a market crash. We are here to help you weigh these options through a transparent, honest conversation that puts your needs before any sales quotas. When you are ready to see how these numbers look for your specific situation, give us a call to start the process.

Practical Considerations: Surrender Charges and Payout Options

The biggest concern we hear from visitors involves liquidity. You might worry that your money will be locked away in a vault for a decade. While an indexed annuity is a long-term commitment, it’s not a financial prison. Most contracts feature a surrender charge schedule lasting between 5 and 10 years. If you withdraw more than the allowed amount during this window, the insurance company applies a penalty. This fee typically starts around 7% or 10% and decreases by 1% each year until it disappears entirely. We recommend matching the annuity term to your specific retirement timeline to avoid these costs.

You don’t have to wait a decade to touch your cash. Almost every carrier includes a "free withdrawal" provision. This allows you to access 10% of your contract value annually without any surrender penalties. If you have a $200,000 account, you can generally take out $20,000 each year for emergencies or travel. This flexibility helps balance the need for growth with the reality of unexpected expenses. It’s a safety valve that provides peace of mind while your principal remains protected from market volatility.

Choosing Your Payout Structure

When you’re ready to turn your savings into checks, you’ll choose a payout method. A lump-sum payout gives you all the cash at once, but you lose the tax-deferred growth and lifetime income guarantees. A "life-only" option provides the highest monthly payment because it stops when you pass away. For couples, we often suggest "Joint and Survivor" options. This structure ensures that a surviving spouse continues to receive payments for the rest of their life. If you want to ensure your heirs receive a benefit, "Period Certain" options guarantee payments for a set timeframe, such as 15 or 20 years, even if you pass away shortly after starting the income stream.

Common Pitfalls to Avoid

A core principle of sound retirement planning is diversification. While annuities provide a secure income stream, many financial advisors suggest allocating capital across different asset classes to balance risk and growth. For those exploring tangible assets, it’s possible to buy residential vacant land nationwide as a path to portfolio growth that is entirely separate from the stock market.

Avoid the mistake of putting every liquid cent into an annuity. We suggest keeping at least 3 to 6 months of living expenses in a standard savings account. Surrender charges are real, and they can eat into your principal if you’re forced to liquidate early. Another protection for prospects is the "Free Look Period." Depending on your state, you have between 10 and 30 days from the date you receive your contract to cancel for a full refund. This gives you time to review the fine print without pressure. Finally, always check the carrier’s financial strength. We recommend looking for companies with an A.M. Best rating of A or higher to ensure they can meet their long-term obligations.

We believe in full transparency regarding the quoting process. If you’re looking for term life insurance, you can get instant quotes on our site without sharing your name, phone number, or email. However, for an indexed annuity or other complex products, such as whole life or disability insurance, we require your contact information up front. These products aren’t one-size-fits-all. We need to have a detailed discussion with you before providing a quote to ensure that the structure aligns with your financial goals. Our experienced independent agents work with you directly to find the right fit for your retirement plan.

Ready to see how a guaranteed income stream fits into your retirement? Speak with an experienced agent today to explore your options.

The LifeInsure Approach: Why We Start with a Discussion

At LifeInsure.com, we believe the quoting process should match the complexity of the specific product you’re researching. If you want term life insurance quotes, our online engine provides them instantly. You don’t have to share your name, phone number, or email address to see those rates. It’s a private, straightforward experience designed for a straightforward product. However, an indexed annuity isn’t a one-size-fits-all solution. It’s a sophisticated financial tool with moving parts like participation rates, spreads, and interest caps that vary significantly between carriers.

For these reasons, we require contact information up front for products such as permanent life insurance, long-term care, or annuities. We’ve found that providing a "blind" quote for these products often leads to confusion or, worse, unsuitable coverage. We must have a detailed discussion with every prospect to ensure the specific indexed annuity structure aligns with their unique retirement timeline and income needs. We act as independent brokers. We don’t work for a specific insurance carrier; we work for you. Our goal is to filter through the noise of 40+ different providers to find the right fit for your capital.

Personalized Guidance vs. Automated Engines

Many websites funnel visitors into massive call centers where the person on the other end might have very little industry tenure. We reject that model entirely. When you request information, we pair you with a dedicated, experienced agent. This professional stays with you from your initial inquiry until your policy is active; you’ll never be passed around to different departments. We evaluate dozens of top-rated carriers to compare current caps and participation rates. This personalized touch is vital for professionals who also require disability insurance quotes or other specialized protections. We look at your entire financial picture to ensure there are no gaps in your safety net.

-

We compare 40+ highly rated insurance companies simultaneously to find the most competitive rates.

-

You receive a dedicated advocate who knows your story, not a rotating cast of call center staff.

-

Our advice is rooted in 29 years of industry experience since our founding in 1995.

-

We prioritize your privacy and never sell or share your data with third-party marketers.

How to Begin Your Annuity Journey

Starting the process is simple but requires a small amount of preparation. We encourage visitors to gather their current retirement account statements and any existing policy documents before we talk. Having these specific numbers ready allows us to provide more accurate projections during our consultation. Our typical introductory call lasts about 15 minutes. During this time, we’ll assess your long-term financial goals and your specific risk tolerance. We won’t pressure you into a decision or use high-stress sales tactics. We’re here to act as educators so you can make a choice that feels secure for your future. If you’re ready to explore your options with an expert, please contact us to schedule your personalized consultation today.

Secure Your Retirement Strategy Today

Finding the right balance between growth and safety doesn’t have to be overwhelming. An indexed annuity offers a unique path to participate in market gains while protecting your principal from 100% of market losses in the 2026 economic landscape. You now understand how participation rates and caps define your potential, and why it’s crucial to plan for surrender periods before you commit. These tools provide a floor for your future that few other vehicles can match.

At LifeInsure.com, we do things differently from a standard call center. While visitors can get term life quotes instantly without sharing a name or email, products like annuities and whole life require us to have a discussion with a prospect before quoting them. We ask for contact information up front for these products because a personalized conversation is the only way to ensure accuracy. This approach allows us to compare 50+ top-rated carriers to find your ideal match. You’ll work directly with one experienced agent from start to finish; we don’t use impersonal call centers. It’s time to move past the guesswork and build a strategy that lasts.

Request a Personalized Permanent Life or Annuity Consultation

Frequently Asked Questions

Can I lose money in an indexed annuity?

You won’t lose your principal due to market performance because an indexed annuity features a 0% floor. This means if the S&P 500 drops 20%, your account balance stays flat rather than falling. You face potential losses only through surrender charges if you withdraw funds during the first 7 to 10 years of the contract, or through optional rider fees you choose to add.

How do insurance companies make money on indexed annuities if they guarantee no losses?

Insurers generate profit by investing your premiums into conservative bonds and keeping the spread between their earnings and your credited interest. They also use caps to limit your gains. For example, if the market rises 12% but your cap is 5%, we keep the remaining 7% to cover costs and manage the 0% loss guarantee. This structure ensures we stay solvent while protecting your savings.

What is the best age to purchase an indexed annuity?

The ideal age to buy is typically between 50 and 70. This window gives you enough time to benefit from tax-deferred growth before you need to start taking distributions. While you can get term life quotes on our site without sharing personal data, we need to speak with you directly for annuity quotes. We require contact information up front so we can tailor the strategy to your specific retirement timeline.

Are indexed annuities considered a good investment for retirement?

An indexed annuity is a reliable choice for prospects who want to protect their nest egg from volatility while still participating in market growth. It’s particularly effective for the 40% of retirees who worry about outliving their savings. Unlike a direct stock investment, it provides a guaranteed income stream that can last for your entire life, regardless of how the underlying index performs during your retirement.

What happens to my indexed annuity if I die before the payout phase?

Your beneficiaries receive the full accumulated value of the contract if you pass away before the payout phase begins. This death benefit typically avoids the costs and delays of probate, which can take 6 to 12 months in many states. We ensure the transition is smooth for your family. Most contracts pay out 100% of the account value directly to your loved ones as a single lump sum.

How are indexed annuities taxed compared to 401(k)s or IRAs?

Annuities offer tax-deferred growth, but the taxation depends on whether you use qualified or non-qualified funds. If you use after-tax money, only the interest earned is taxed at your ordinary income rate upon withdrawal. This differs from a traditional 401(k) where 100% of the distribution is taxable. We help visitors understand these nuances during our initial consultation to ensure there are no tax surprises when you begin your withdrawals.

Can I roll over my existing 401(k) into an indexed annuity?

You can certainly roll over 401(k) funds into an annuity through a tax-free direct rollover process. We frequently handle these requests for prospects seeking to secure their gains. Unlike our instant term life engine, we require contact info up front for this product. We need to have a detailed discussion with you first to ensure that the rollover complies with all IRS regulations and aligns with your long-term financial goals.

What is a ‘buffer’ in a registered index-linked annuity (RILA)?

A buffer is a level of protection in which the insurer covers a set percentage of market losses, such as the first 10% or 20%. If the market drops 15% and you have a 10% buffer, your account only loses 5%. This differs from a standard indexed annuity, which protects you from losses. These products offer higher growth caps in exchange for you accepting a small amount of downside risk.

Last Updated on April 16, 2026 by Richard Reich