If you turned in your badge tomorrow, would your family’s financial safety net stay behind at the precinct? We know that relying solely on department-issued benefits feels like a gamble. Most of the 800,000 law enforcement officers serving in the U.S. find that these policies don’t follow them if they change departments or retire. Finding private life insurance for police officers often feels frustrating when you’re hit with high-risk premiums or invasive quote forms that demand your personal data before you even see a price.

We promise to show you how to bridge that gap while protecting your privacy and your pocketbook. You can get instant term life quotes on our site without entering your name, phone number, or email address. For more complex needs like disability insurance or whole life, we’ll need to speak with you directly. This conversation ensures our experienced agents provide an honest, accurate quote tailored to your specific role. You’ll discover how to build a portable plan for 2026 that secures your family’s future, no matter where your career leads.

Key Takeaways

- Understand the critical differences between group term life and private policies to ensure your family isn’t left with a dangerous coverage gap.

- Navigate the underwriting process by learning how “hazardous occupation” ratings and flat extra fees impact your monthly premiums.

- Protect your privacy by using our anonymous quote engine to see ballpark rates for life insurance for police officers without sharing your personal contact information.

- Learn why complex products like disability and permanent life insurance require a direct consultation with our experts to ensure your financial safety net is built correctly.

- Discover the advantages of working with an independent brokerage that specializes in placing high-risk law enforcement cases with the right carriers.

Assessing Your Current Coverage: Why Department-Issued Life Insurance May Not Be Enough

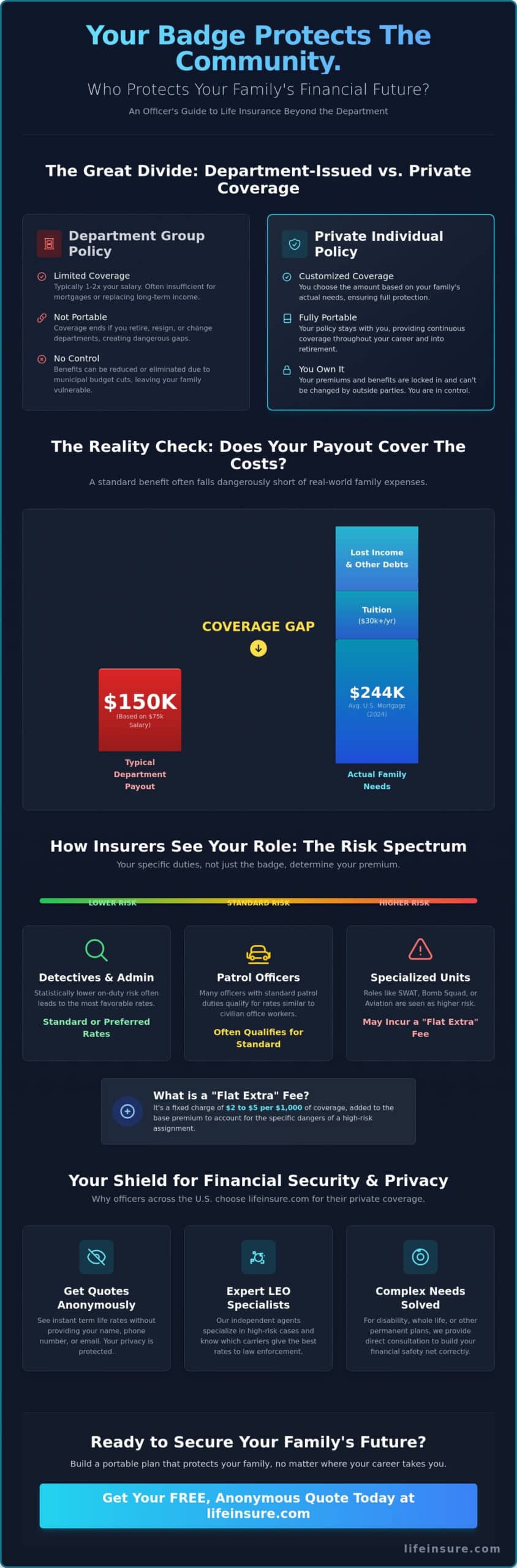

We know that your primary focus is protecting the community, but protecting your own home requires a different strategy. Most law enforcement agencies provide a basic group term policy as part of your benefits package. This department-issued life insurance is a helpful start, but it often functions as a safety net with large holes. Group policies are generally “one size fits all” and don’t account for your specific debts or family goals. While we offer term life insurance quotes instantly without requiring your name or phone number, we find that many officers rely too heavily on their workplace coverage without seeing the full picture.

Standard agency coverage typically follows a “salary multiple” formula. In 2024, most departments offer a payout equal to one or two times your annual salary. If you earn $75,000, a $150,000 benefit might sound substantial, but it rarely covers a modern mortgage and years of lost income. Relying on these benefits is also becoming riskier. As municipal budgets tightened in 2025, some cities began auditing “fringe benefits” to cut costs. This means your future coverage stability rests in the hands of local government officials rather than your own.

The Portability Trap: What Happens to Your Coverage When You Leave the Force?

Group life insurance is usually tied to your active employment. If you resign, retire, or take a lateral move to a different agency, your coverage often vanishes. This creates a dangerous window of vulnerability. We’ve seen officers wait until retirement to seek private life insurance for police officers, only to find they’ve developed high blood pressure or other job-related health issues. These changes can make you uninsurable or drive your premiums much higher. Securing a private policy now ensures you’re protected regardless of your badge status.

Coverage Gaps: Is a Basic Benefit Sufficient for Your Family’s Needs?

Real-world expenses quickly outpace a standard department payout. With the average U.S. mortgage balance hovering around $244,000 in early 2024, a basic salary multiple barely clears the house debt, let alone credit cards or funeral costs. Law enforcement families with children also face the rising cost of tuition, which can exceed $30,000 per year at many state universities. Supplemental coverage acts as the bridge between basic survival and long-term security. For more complex needs like whole life, we require a direct conversation to ensure the policy fits your financial legacy, as these products involve more intricate planning than a standard term quote.

Navigating Underwriting: How Law Enforcement Risks Affect Your Premiums

We understand that your badge comes with unique responsibilities that the average civilian never faces. When you apply for life insurance for police officers, insurance companies evaluate your daily duties through a lens of risk management. Most carriers classify law enforcement as a hazardous occupation, but this label does not automatically mean you will pay high premiums. In fact, many patrol officers who work standard shifts qualify for standard or even preferred rates similar to office workers.

Some carriers apply what is known as a flat extra fee to policies for individuals in high-risk roles. This is a set dollar amount, typically ranging from $2 to $5 per $1,000 of coverage, added to your base premium. It accounts for the specific dangers of your assignment rather than your physical health. You can find more details on how companies handle underwriting for high-risk occupations to see how these fees are calculated across the industry.

Being transparent about your assignment is vital. If you work in a specialized unit but claim to be a desk sergeant, a future claim could be denied for material misrepresentation. We help you navigate these disclosures so your family remains protected no matter what.

Specialized Units and Risk Classifications

Underwriters distinguish between different roles within the department. A detective or an administrative officer usually receives the most favorable rates because their on-duty risk is statistically lower. Conversely, members of a bomb squad, SWAT team, or aviation unit may face higher premiums due to the specialized nature of their work. We work with officer-friendly carriers that recognize the training and safety protocols these units follow, which can often mitigate the perceived risk. We also look at your off-duty lifestyle, as hobbies like SCUBA diving or private piloting can impact your rating just as much as your job.

Health vs. Occupation: What Matters More to Underwriters?

It might surprise you to learn that your blood pressure and BMI often carry more weight than your badge. According to 2024 industry data, health-related factors account for approximately 75 percent of a rating decision. An officer in excellent physical shape who works a high-risk beat may actually pay less than a sedentary administrator with high cholesterol. To get the best results, we recommend having this information ready:

- Current height and weight measurements

- Recent blood pressure and cholesterol readings

- A list of any medications you currently take

- Specific details of your unit or specialized training

If you want to see how affordable your coverage can be, you can get term life insurance quotes instantly on our site without entering your name, phone number, or email. For more complex products like disability insurance or whole life, we will need to speak with you directly to gather specific details before providing an accurate quote.

Beyond Death Benefits: Disability and Permanent Life Insurance for Officers

A solid financial plan involves more than just preparing for the unthinkable. While life insurance for police officers provides a vital safety net for your family, it’s only one piece of the puzzle. True financial security means protecting your ability to earn an income today while building assets for tomorrow. We distinguish between term life insurance, which offers temporary protection during your working years, and permanent life insurance, which provides lifelong coverage and a growing cash component.

Most officers rely heavily on department-issued policies. However, these are often capped at low multiples of your salary and don’t move with you if you change agencies or retire. By looking beyond simple death benefits, you can create a strategy that handles injuries, long-term illness, and retirement gaps. This requires a consultative approach. Because these products are more complex than basic term policies, we need to speak with you directly to ensure the coverage aligns with your specific pension and benefit structure.

Protecting Your Income with Disability Insurance

Statistically, you’re more likely to face a career-ending injury than a premature death. Data from the Bureau of Labor Statistics shows that police officers experience some of the highest rates of nonfatal on-the-job injuries of any profession. If a back injury or a physical altercation leaves you unable to perform your duties, your department’s disability benefits might only cover a fraction of your take-home pay. This is why “own-occupation” definitions are critical. This specific language ensures you receive benefits if you can’t work as a police officer, even if you’re healthy enough to work a desk job elsewhere.

We want to help you secure your paycheck, but providing accurate disability insurance quotes requires a brief conversation. Unlike term life, disability rates depend heavily on your specific unit, daily duties, and current health status. We need to understand your existing department benefits first so we don’t over-insure you or leave you with a dangerous coverage gap.

Permanent Life Insurance: Building Cash Value for Retirement

While term life is excellent for affordable, high-limit protection, permanent life insurance serves a different purpose. Policies like Whole Life or Universal Life act as a supplemental retirement vehicle. These plans build cash value over time, which grows on a tax-deferred basis. For many officers, this cash value acts as a “private bank” that you can access for emergencies or use to fund a child’s education without the restrictions of a 457(b) or 401(k) plan.

Choosing the right permanent life insurance for police officers involves analyzing your long-term goals and budget. These permanent life insurance policies are highly customizable, which is why our quote request process requires your contact information. We don’t believe in one-size-fits-all solutions. An experienced agent will work with you to structure a policy that balances your need for a death benefit with your desire to accumulate accessible wealth for your post-patrol life.

Shopping for Life Insurance Without Compromising Your Privacy

Finding the right life insurance for police officers shouldn’t feel like a high-stakes investigation. We’ve streamlined the shopping experience into a transparent, four-step process. This approach ensures you get the coverage you need without the typical industry headaches. Our process makes securing life insurance for police officers simple and secure.

- Step 1: Determine your coverage amount. Use a needs-analysis approach to calculate your family’s requirements. This includes your mortgage balance, existing debts, and future education costs for children. A common benchmark is 10 to 15 times your annual salary.

- Step 2: Use an anonymous quote engine. You can view ballpark term rates instantly. We provide these figures without requiring your identity upfront.

- Step 3: Compare carriers side-by-side. Look at multiple top-rated companies at once. This allows you to see how different insurers treat the specific risks associated with law enforcement.

- Step 4: Connect with an independent agent. Reach out only when you’re ready to apply. We stay with you from the first form to the final policy delivery.

The Problem with Traditional Lead Generation

Many insurance websites exist solely to harvest and sell officer data. Once you hit submit, your contact info is often auctioned to dozens of aggressive telemarketers. This leads to a constant stream of spam calls and emails that interrupt your rest or your shift. We find this practice disrespectful to first responders. Our commitment is simple: we never sell or share your personal info. You control the pace of the conversation. We don’t believe in high-pressure sales tactics.

How to Compare Term Quotes Anonymously

We’ve developed a specialized system for term life insurance quotes that protects your identity. You can see real numbers from various carriers without entering a name, phone number, or email. This empowers you to shop without pressure. It’s a direct contrast to the impersonal call center model used by large aggregators where you’re just another number in a queue.

While we offer anonymous quoting for term life, more complex products require a different approach. If you’re interested in disability insurance, whole life, or long-term care, we’ll need to speak with you directly. These policies are highly customized. We must conduct a direct discussion with every prospect to provide accurate figures and ensure the policy meets your specific needs. We’re upfront about this because we value your time and want to get the details right the first time.

Ready to see your options without the sales pressure? Get your anonymous term life quotes now.

Why Police Officers Choose LifeInsure.com for Private Coverage

We understand that law enforcement isn’t just a job; it’s a commitment that carries unique risks. While many officers rely solely on department-issued plans, we help you build a private safety net that stays with you even if you change careers or retire. In 2026, the landscape of life insurance for police officers continues to evolve, and we stay ahead of these changes to ensure your family remains protected.

Independent Brokerage vs. Captive Agents

We aren’t tied to a single insurance company. Instead, we act as an independent brokerage. This means we represent you, not the carrier. While a captive agent can only offer one company’s rates, we shop over 40 top-rated carriers to find the best fit for your specific health profile and job duties. We advocate for you during the medical underwriting process. If a carrier has concerns about your patrol duties or high-risk assignments, we know which companies view those roles more favorably. For a full look at the current market, you can access term life insurance quotes instantly. We don’t require your name, email, or phone number to see these rates.

Transparent Consultations for Complex Needs

Some financial goals require more than a basic policy. If you’re considering products like Whole Life, disability insurance, or long-term care, the process is more detailed. These products aren’t one-size-fits-all. Because of this complexity, we require a direct conversation before providing quotes. We prioritize an experienced agent’s guidance for these plans to ensure your coverage is structured correctly. Our goal is education. We want you to make an informed decision at your own pace without feeling pressured.

Working with us means you get a single-agent experience. You won’t be bounced around an impersonal call center. You’ll have one dedicated professional who understands the nuances of life insurance for police officers and stays with you from the first call to the final signature. This personalized approach ensures your policy is handled with the respect and attention your service deserves.

Don’t leave your family’s future to chance with a policy that expires when you turn in your badge. Secure a portable, private plan that provides peace of mind throughout your career and into retirement. Contact us today to start your consultation and take the next step toward a secure financial future.

Protect Your Family With Privacy and Precision

We’ve shown that relying solely on department-issued benefits often leaves your family’s future at risk. Securing life insurance for police officers requires a strategy that accounts for specific occupational hazards while keeping your sensitive information secure. We’ve built our platform to give you total control over this process. You can explore quotes from 40+ top-rated carriers through our site today.

If you’re interested in term life insurance, you can Get Instant Term Life Quotes Anonymously without providing a name, phone number, or email address. For complex products like disability insurance, whole life, or long-term care, we’ll need to speak with you directly. These policies require a detailed consultation with each prospect to ensure every detail of your law enforcement career is properly underwritten. You’ll work one-on-one with an experienced independent agent who understands your profession, ensuring you never have to deal with an impersonal call center. It’s about getting the honest protection you’ve earned. We’re ready to help you build a secure foundation for the years ahead.

Frequently Asked Questions

Is life insurance more expensive for police officers?

Most police officers qualify for the same competitive rates as the general public because modern actuarial data shows that law enforcement is safer than many people realize. According to the Bureau of Labor Statistics 2023 data, the fatal injury rate for officers is lower than that of loggers or roofers. We help you find carriers that view your service as a manageable risk, ensuring your premiums remain affordable.

Can I get life insurance if I am in a specialized high-risk unit like SWAT?

You can definitely secure coverage while serving in a specialized unit like SWAT, Bomb Squad, or K-9. Some insurance companies may add a “flat extra” fee, which is a specific dollar amount per $1,000 of coverage, to account for the increased tactical risk. We work with 40 different carriers to identify those that offer the most favorable terms for high-risk assignments without charging excessive premiums.

What happens to my life insurance if I retire or change departments?

Your private life insurance policy remains in force regardless of your employment status as long as you continue to pay the premiums. Unlike department-issued group coverage, which 95% of the time terminates when you hang up the badge, an individual policy is portable. It stays with you if you transition to a private security role or enter full retirement in 2026, providing permanent peace of mind.

Do I need to provide my social security number just to get a quote?

We don’t require your social security number, name, or phone number to provide instant term life insurance quotes. You can compare rates from top-rated carriers anonymously on our website to see how affordable life insurance for police officers can be. We believe in a privacy-first approach that lets you shop for basic coverage without the pressure of immediate sales calls or data sharing.

Is the life insurance provided by my police union enough?

Union or department-provided group policies are rarely enough because they typically offer a death benefit equal to only 1 or 2 times your annual salary. Financial experts often recommend a benefit that is 10 to 15 times your income to fully protect your family’s future. Supplementing your union coverage with a private policy ensures your loved ones have a secure financial cushion that isn’t tied to your job.

Can I get life insurance without a medical exam as a first responder?

Many first responders qualify for no-exam or accelerated underwriting policies that use digital health records to approve coverage in minutes. If you’ve had a physical in the last 12 to 24 months, you might bypass the needle and the blood pressure cuff entirely. This process is fast and easy for officers with clean medical histories who need to secure their family’s future quickly.

Why do I need to talk to an agent for disability insurance quotes?

We require a direct conversation before providing disability insurance quotes because these policies are highly complex and depend on your specific job duties. Unlike term life, disability coverage requires us to define “own-occupation” versus “any-occupation” based on your specific unit and daily tasks. We need your contact information upfront to ensure an experienced agent can build a quote that actually protects your paycheck.

What is the best type of life insurance for a young police officer?

Term life insurance is usually the best choice for young officers because it provides the largest death benefit for the lowest monthly cost. A 20 or 30-year term covers your most vulnerable years, such as when you’re paying off a mortgage or raising children. While we also offer whole life for those seeking permanent coverage, term life provides the straightforward protection most young families need to stay secure.

Last Updated on April 29, 2026 by Richard Reich