Let’s be honest: shopping for life insurance can feel overwhelming. You worry it’s too expensive, that finding cheap life insurance means you’re getting a bad deal, and that the moment you ask for a quote, your phone will start ringing off the hook. It’s a common frustration, but protecting your family shouldn’t be this complicated or stressful. The truth is, high-quality coverage is more affordable than you may realize, and you deserve to explore your options without any pressure.

In this 2026 guide, we’ll cut through the noise. We will show you exactly how to find affordable, high-quality coverage from trusted companies. You will learn the actionable strategies our experienced agents use to lower premiums, understand the key factors that actually influence your rates (even with health concerns), and discover how to get real, honest quotes without ever sharing your name, phone number, or email. It’s time to make an educated decision and find the peace of mind you deserve, without the high price tag.

What ‘Cheap’ Life Insurance Really Means: Price vs. Value

When searching for financial protection for your family, the term ‘cheap’ can feel a bit unsettling. Let’s be clear: when we talk about finding cheap life insurance, we don’t mean low-quality or unreliable. We mean securing a high-value life insurance policy that fits comfortably within your budget.

The goal isn’t just to find the lowest possible price-it’s to secure the lowest price for the right amount of coverage your loved ones need. A common myth is that an inexpensive policy won’t pay out, but this is simply not true. As long as you purchase from a reputable, financially stable carrier and are honest on your application, your policy is secure. Your final premium will always depend on personal factors like your age, health, and lifestyle, not just the company you choose.

Term Life Insurance: The Foundation of Affordability

For most families, the most straightforward path to affordable coverage is a term life policy. Unlike whole life insurance, which is designed to last a lifetime and includes a complex cash-value investment component, term life is simple and significantly more affordable.

-

It covers a specific period: You choose a term, typically 10, 20, or 30 years (sometimes 35 or 40 years), to cover the years your family needs protection most.

-

It’s pure protection: There are no investment fees or cash value accounts, keeping premiums low.

-

Maximum benefit, minimum cost: It provides the largest possible death benefit for the lowest monthly premium.

Finding Value: Looking Beyond the Monthly Premium

The most affordable quote isn’t always the best one. True value comes from a combination of price, carrier strength, and policy flexibility. Before you buy, always consider the insurer’s financial strength rating from an agency like A.M. Best, which indicates its long-term ability to pay claims.

Additionally, look for valuable features that can enhance your coverage. Policy riders, often available for a small additional cost, can add benefits such as waiving premiums if you become disabled. A conversion option is another key feature, giving you the flexibility to convert your term policy to a permanent policy later without requiring a new medical exam.

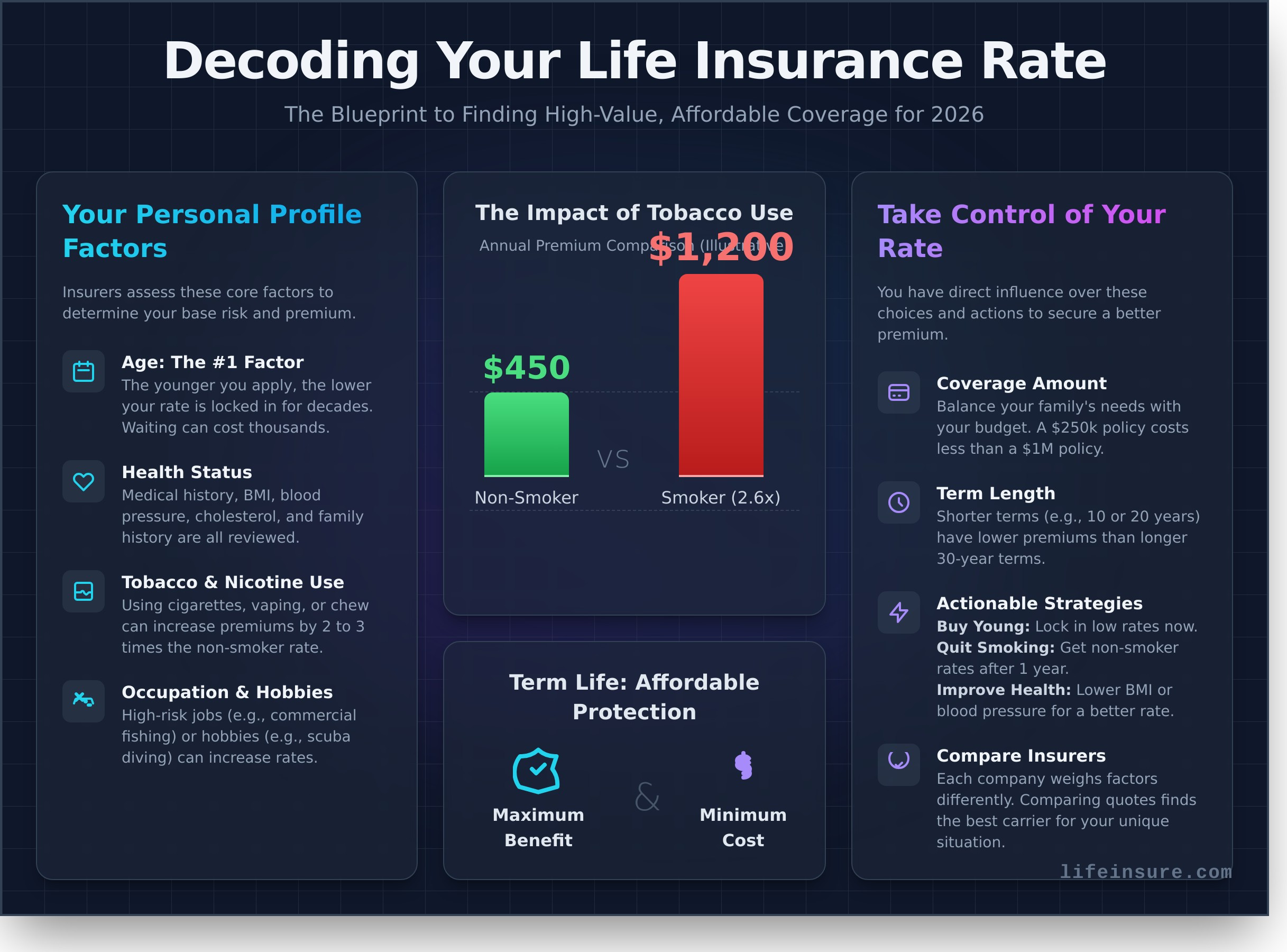

The 5 Key Factors That Determine Your Life Insurance Rates

Ever wonder what happens behind the scenes when you get a life insurance quote? Insurers use a detailed process called underwriting to assess your personal risk and set your final premium. Understanding the factors they consider helps you find the most affordable coverage. Think of these not as roadblocks, but as levers you can either control or understand to secure the best possible rate.

Personal Factors: Your Health and Lifestyle

This is all about you. Insurers build a risk profile based on your personal data, which directly correlates with life expectancy. The lower the risk, the lower your price.

-

Age: This is the single most important factor. The younger and healthier you are when you apply, the lower your rate will be. Locking in a rate in your 30s can save you thousands over the life of the policy compared to waiting until your 50s.

-

Health: Underwriters will review your medical history, current conditions like high blood pressure or diabetes, family health history, and your height-to-weight ratio (BMI).

-

Tobacco Use: If you use nicotine in any form-cigarettes, vaping, or chewing tobacco-expect to pay significantly more. Smokers often pay two to three times the premium of a non-smoker for the exact same coverage.

-

Hobbies & Occupation: A dangerous job (such as commercial fishing) or high-risk hobbies (such as scuba diving or private piloting) can increase your rates.

Policy Factors: Your Coverage Choices

The second part of the equation is determined by the specific policy you build. You have direct control over these choices, which allows you to balance your budget with your family’s needs.

-

Coverage Amount: This is the death benefit paid to your beneficiaries. A $1,000,000 policy will naturally cost more than a $250,000 policy.

-

Term Length: The duration of your coverage. A shorter 10-year term policy is less expensive than a 30-year term because the insurer’s period of risk is shorter.

-

Policy Type: Term life is the most straightforward and affordable option. For a deeper, unbiased look at how different policies work, the NAIC consumer guide is an excellent resource. Permanent policies, such as whole life, are more complex and cost significantly more.

Don’t worry if you have a few risk factors. The key to finding cheap life insurance is understanding that every company weighs these factors differently. One insurer might be more lenient with a past health issue, while another may offer better rates for your specific occupation. That’s why comparing quotes is so important-it helps you find the carrier that is the best fit for your unique situation.

7 Actionable Strategies to Get Cheaper Life Insurance Premiums

Finding affordable life insurance doesn’t have to be complicated. While factors like age and health play a big role, you have more control over your final premium than you might think. By being a proactive, informed shopper, you can significantly reduce your costs. Here are seven actionable strategies to help you secure truly cheap life insurance coverage.

Timing and Health Improvements

Your health profile is the foundation of your life insurance rate. Taking steps to improve it-even small ones-can lead to big savings.

-

1. Buy Young: The single best time to buy life insurance is now. Rates are lowest when you are young and healthy. Applying in your 30s instead of your 40s can lock in a significantly lower premium for decades to come.

-

2. Quit Smoking: This is the fastest way to slash your premiums. Insurers charge smokers and tobacco users two to three times more than non-smokers. Most companies will offer non-smoker rates after you’ve been nicotine-free for at least one year.

-

3. Improve Your Health: Insurers reward proactive health management. Lowering your blood pressure, losing weight to achieve a healthy BMI, or managing your cholesterol can move you into a better rate class and lower your price.

Smart Policy Structuring

How you build your policy is just as important as your health. Don’t pay for more coverage or a longer term than you actually need.

-

4. Choose the Right Term Length: A 30-year policy isn’t always the best choice. Align your term length with your biggest financial obligation, such as a 15-year mortgage or the 20-year period until your children are independent. Understanding your options is key, and this consumer guide to life insurance from the National Association of Insurance Commissioners (NAIC) can help clarify your needs.

-

5. Consider Laddering Policies: Instead of one large policy, you can "ladder" multiple smaller policies with different term lengths. This allows your coverage to decrease as your financial responsibilities shrink over time, saving you money.

-

6. Pay Annually: If you can, pay your premium once a year instead of monthly. Most insurers offer a small discount (typically 3-5%) for annual payments, as it reduces their administrative costs.

The Most Important Strategy: Compare, Compare, Compare

7. Shop the Market: This is the single most effective way to ensure you get the lowest price. Rates for the exact same person can vary by 50% or more between insurance companies. Why? Because every insurer assesses risk differently. One company might be more lenient with high cholesterol, while another offers better rates for well-managed diabetes.

By comparing quotes from dozens of top-rated carriers, you can find the one that views your specific health and lifestyle profile most favorably. This simple step guarantees you aren’t overpaying.

Ready to see how these factors affect your price? Get an instant, anonymous quote.

Finding the Most Affordable Policy for Your Situation

The term "cheap life insurance" means different things to different people. The most affordable policy for a healthy 30-year-old is not the same as the best-value option for a 65-year-old with a health condition. The key is to match the right policy type to your specific needs, budget, and health profile. Understanding your options is the first step toward securing financial peace of mind without overpaying.

Let’s break down the most common types of affordable life insurance to help you find your perfect fit.

Standard Term Life: For Most Families on a Budget

For most people, standard term life insurance is the most cost-effective way to protect their family’s financial future. It provides a large amount of coverage for a set period (the "term"), typically 10, 20, or 30 years. This makes it the ideal, straightforward solution for covering temporary, high-cost needs like:

-

Replacing your income until your children are grown

-

Paying off a mortgage

-

Covering outstanding private student loans or other debts

For those who need coverage quickly, no-exam term life offers a faster application process, though it sometimes comes with a slightly higher premium.

Final Expense Insurance: For Seniors Covering End-of-Life Costs

Also known as burial insurance, this is a small whole-life policy designed to cover costs associated with a funeral, cremation, and other final expenses. Because coverage amounts are typically between $5,000 and $40,000, monthly premiums are very manageable. Most final expense policies feature simplified underwriting, meaning you only have to answer a few health questions, and no medical exam is required.

Guaranteed Issue Life Insurance: When Health is a Major Concern

If you have been declined for other types of life insurance due to serious health issues, a guaranteed issue policy is a valuable option. As the name implies, your acceptance is guaranteed. You cannot be turned down for health reasons. In exchange for this guarantee, these policies have higher premiums for their coverage amount and include a graded death benefit. This typically means if death occurs from natural causes in the first two years, your beneficiary receives the premiums you paid, plus interest, rather than the full policy amount.

The best way to find truly cheap life insurance is to compare quotes tailored to you. At LifeInsure.com, our experienced agents can help you navigate these options to make a confident, educated decision.

How to Compare Cheap Life Insurance Quotes The Smart Way

Now that you understand the essentials of affordable coverage, the final step is to compare quotes. But the way you shop is just as important as the policies you consider. To find the best rates and avoid hassles, it’s crucial to understand the difference between a captive agent and an independent broker.

A captive agent represents a single insurance company, meaning they can only offer you that one company’s products-whether or not they’re the best fit for you. An independent broker, like the experienced agents at LifeInsure.com, works for you. This distinction is the key to unlocking real savings.

Why Independent Brokers Find Cheaper Rates

An independent broker’s sole mission is to find you the best policy at the most competitive price, period. We aren’t tied to any single carrier. Instead, we leverage our access to the entire market to create a bidding war for your business. This gives you three powerful advantages:

-

We work for you. Our loyalty is to our clients, not an insurance company. We provide unbiased advice tailored to your needs.

-

We shop dozens of carriers at once. You provide your information once, and we instantly compare rates from top-rated insurers to find the lowest premium.

-

We have insider knowledge. We know which companies offer the best rates for specific health conditions or lifestyles. This expertise is essential for finding genuinely cheap life insurance if you’re not in perfect health.

The Power of Anonymous Quoting

We believe shopping for life insurance should be simple and secure. The biggest frustration for many people is receiving unsolicited sales calls and emails after requesting a quote. We’ve built our entire process to eliminate that problem.

Our free online tool lets you see real, accurate rates from the nation’s best insurance companies in under a minute. And we stand by our "Privacy First" promise: you never have to provide your name, phone number, or email to see your personalized quotes. This puts you in complete control of the process, free from any sales pressure.

You get the honest information you need without sacrificing your privacy. Ready to see how affordable peace of mind can be?

See for yourself. Compare quotes in 60 seconds.

Finding Your Best Rate is Easier Than You Think

You’re now equipped with the knowledge to find life insurance that’s both affordable and high-quality. Remember, the key is to look beyond the price tag and focus on value. By understanding the factors that influence your rates and applying the strategies we’ve discussed, you can confidently navigate the process. The search for genuinely good, cheap life insurance doesn’t have to be complicated or stressful.

The best way to put this knowledge into action is to see your real numbers. We make it simple, private, and secure. Compare instant, anonymous life insurance quotes now and see prices from dozens of A-rated companies without entering your name or phone number. When you’re ready for guidance, you’ll work with an experienced agent-never a call center-to find the perfect fit for your needs.

Securing your family’s financial future is one of the most powerful steps you can take. You’re now ready to make an educated decision and find the peace of mind you deserve.

Frequently Asked Questions About Cheap Life Insurance

What is the average cost of cheap life insurance per month?

The cost varies based on your age, health, and coverage amount, but it is more affordable than most people think. For example, a healthy 35-year-old can often secure a 20-year term policy with $500,000 in coverage for around $25 to $40 per month. The best way to find your specific rate is to get an instant quote, which lets you compare honest options from top-rated carriers with no commitment.

Can I get affordable life insurance if I smoke or have a medical condition?

Yes, it is absolutely possible. While premiums will be higher than for someone in perfect health, different insurance companies evaluate health conditions differently. Some are more lenient with specific issues than others. An experienced independent agent can help you navigate these options by discreetly shopping your case to identify the carrier that offers the most favorable rating and the most affordable premium for your unique situation.

Is term life insurance always the cheapest option?

For most people, term life insurance is the most cost-effective option. It offers the largest death benefit at the lowest premium because it covers you for a specific period (such as 10, 20, or 30 years) and doesn’t build cash value. This makes it the ideal solution for anyone seeking affordable, pure life insurance coverage to protect their family during their most critical financial years, such as when raising children or paying a mortgage.

How can I be sure a cheap life insurance company is legitimate and will pay out?

The most reliable method is to check a company’s financial strength rating from an independent agency like A.M. Best. A rating of "A" (Excellent) or higher signifies a strong, long-term ability to pay claims. We are committed to representing only financially secure, highly rated insurance carriers, so you can be confident that the policy you choose is backed by a dependable company that will be there for your family when they need it most.

What happens if I can no longer afford my life insurance premiums?

The most important thing is not to let the policy lapse. Contact your agent immediately, as you likely have several options. You may be able to reduce your coverage amount to lower your monthly premium to a more manageable level. It is always better to have some coverage than none. Being proactive allows you to explore all available solutions to keep your family protected without causing financial strain.

Does getting a quote affect my credit score?

No, getting a life insurance quote has zero impact on your credit score. When you formally apply, insurers may perform a "soft inquiry" to verify information, but this is not visible to lenders and does not affect your rating. You can get initial quotes from us without providing any personal contact information, giving you a secure, pressure-free way to explore your options and see how affordable coverage can be.

Last Updated on April 16, 2026 by Richard Reich