A diagnosis of Chronic Kidney Disease (CKD) is often viewed as an automatic “no” from insurance companies, but that assumption is simply outdated. We understand the anxiety that comes with sharing your health history, especially when you’re worried about being rejected. Securing life insurance with kidney disease is entirely possible in 2026, provided you match your specific health stage with the right carrier.

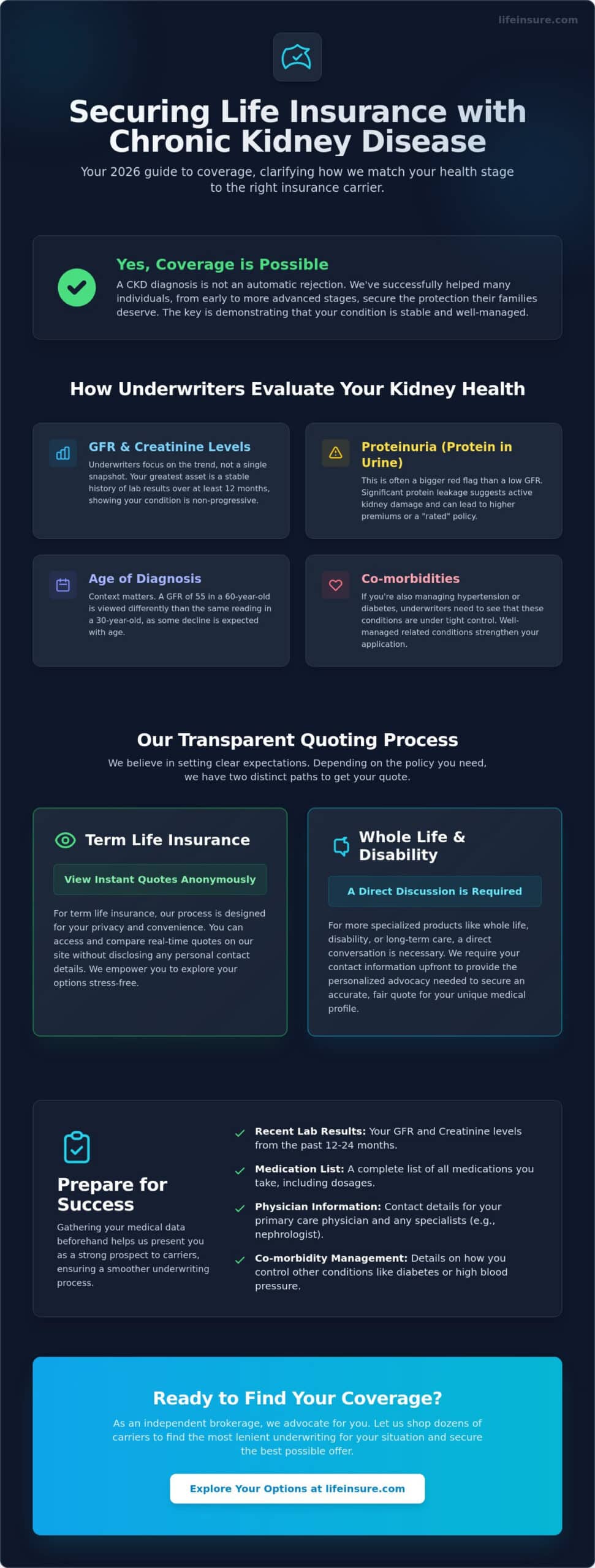

We believe in a transparent, stress-free process. If you’re looking for term life insurance, you can access quotes on our site without disclosing personal contact details. For more specialized products like whole life, disability insurance, or long-term care, we require your contact information upfront. This is because a direct discussion is necessary to understand your unique medical profile before we can provide an accurate quote. This consultative approach allows us to advocate for you as a prospect, ensuring your GFR and creatinine levels are explained correctly to underwriters.

In this guide, we’ll help you navigate the underwriting process for every stage of CKD. You’ll learn which policies offer the best value for your situation and how to find a carrier that views your health management as a priority. Let’s clear up the confusion and get you the coverage you deserve.

Key Takeaways

- Most individuals with CKD can qualify for coverage, though your specific health stage and stability determine which policy types are available.

- Learn how underwriters evaluate your GFR and creatinine levels to set premiums for life insurance with kidney disease.

- Understand the difference between viewing term life rates anonymously and the direct discussion we require for complex products like whole life or disability insurance.

- Gather your recent medical data using our checklist to ensure you’re presented as a strong prospect to potential carriers.

- Discover how an independent brokerage advocates for you by shopping dozens of carriers to find the most lenient underwriting for your situation.

Can You Get Life Insurance with Kidney Disease?

The short answer is yes. Many people assume that a diagnosis of Chronic Kidney Disease (CKD) creates an immediate barrier to financial protection, but that isn’t the reality in 2026. We’ve helped many individuals secure life insurance with kidney disease, ranging from those in the earliest stages to those managing more advanced cases. The key isn’t having perfect health; it’s demonstrating that your condition is stable and well-controlled through regular medical follow-ups.

Insurers view kidney health as a spectrum. While a diagnosis matters, the specific stage of your disease and your overall health trajectory are what truly drive the underwriting decision. We see successful approvals every day for applicants with Stage 1, 2, and even Stage 3 CKD. The goal is to match your unique medical profile with the carrier most likely to offer favorable terms.

Understanding the Underwriting Spectrum

Insurance companies don’t expect every applicant to be in peak physical condition. Instead, they view kidney disease as a manageable risk if your lab results remain consistent. When you’re understanding chronic kidney disease (CKD), it becomes clear that insurers aren’t looking for a cure, but rather evidence that the condition is non-progressive. If your health is excellent otherwise, you might qualify for “Standard” rates. If there are minor complications, you may receive a “substandard” or “rated” policy. This simply means the premium is slightly higher to account for the increased risk, but coverage remains fully available to protect your family.

When is Life Insurance Most Accessible?

Applicants in Stage 1 and Stage 2 CKD often have the widest variety of options. Underwriters look for a “green flag,” which is typically a stable Glomerular Filtration Rate (GFR) for at least 12 months. If your GFR and creatinine levels haven’t fluctuated significantly, you’re in a strong position. We also look at co-morbidities. If you’re managing hypertension or diabetes alongside kidney issues, underwriters will want to see that those conditions are also under tight control.

We believe in setting clear expectations for every prospect. If you’re interested in a term life policy, you can explore quotes on our platform without sharing personal contact details. However, for more complex needs like whole life, disability insurance, or long-term care, we’ll need to have a direct discussion. These products require a deeper look at your medical history to ensure we find the right fit. We’ll ask for your contact information upfront so we can provide the personalized advocacy required to secure an accurate, fair quote.

How Underwriters Evaluate Kidney Health

When applying for life insurance with kidney disease, the underwriting process is more rigorous than a standard application. Carriers don’t just look at the diagnosis; they analyze the functional capacity of your kidneys. Underwriters prioritize your Glomerular Filtration Rate (GFR) and Creatinine levels to determine your risk class. While a single lab result provides a snapshot, insurance companies are far more interested in the trend of these numbers over time. Stability is your greatest asset during this evaluation.

Proteinuria, or protein in the urine, is often a bigger red flag than GFR alone. If your GFR is slightly low but you have no protein in your urine, underwriters may view your case more favorably. Conversely, significant protein leakage suggests active damage, which can lead to higher premiums or a “table rating.” The age at which you were diagnosed also matters. Underwriters view a 60 year old with a GFR of 55 differently than a 30 year old with the same reading, as some decline is expected with natural aging.

It is also vital to distinguish between chronic failure and isolated issues. A history of kidney stones or benign tumors is handled differently than chronic kidney disease. If your stones were a one-time event or your tumors were found to be non-cancerous and haven’t affected function, you might still qualify for standard rates. You can explore term life insurance quotes on our site without sharing personal data to see how these factors might impact your potential costs.

Key Metrics: GFR and Creatinine Levels

GFR is the primary gauge of kidney filtration efficiency used by all major carriers. Stages 1 and 2 are typically considered “mild” and often result in standard or near-standard approvals. Stage 3 is where “table ratings” usually begin, meaning you’ll pay a percentage more than the standard rate. Underwriters look for trends in Creatinine rather than a single reading to ensure your kidneys aren’t actively declining. A stable Creatinine level over 12 to 24 months demonstrates that your condition is well-managed.

The Role of Underlying Causes

The cause of your kidney issues is just as important as the numbers. Underwriters differentiate between CKD caused by natural aging and conditions like Polycystic Kidney Disease (PKD), which is progressive. Well-managed blood pressure can often offset a lower GFR rating because it shows you are proactively protecting your renal health. Your nephrologist’s notes are the most important document in your file, as they provide context that raw lab data lacks. For a detailed look at the clinical side, you can research kidney disease diagnosis and treatment to see what your doctor reports to the insurance company.

We believe in maintaining a consultative brand voice to help every prospect. If you need complex coverage like whole life, disability insurance, or long-term care, we require your contact information upfront. This is because a direct discussion is necessary to advocate for your specific health situation before we can provide accurate pricing. You can contact us today to start that conversation and find the best path forward.

Choosing the Right Policy: Term vs. Permanent Coverage

Selecting the right policy requires a careful balance between your family’s financial needs and your current health status. For many applicants, life insurance with kidney disease is most accessible and affordable when structured as a term policy, particularly for those in the early stages of CKD. We want you to feel empowered throughout this process, knowing that a diagnosis doesn’t mean you’re restricted to a single, expensive option. Whether you need a temporary safety net or lifelong protection, the key is understanding how your health stage influences the application workflow.

Term Life: Fast and Anonymous Quotes

Term life insurance is often the best entry point if you’re in Stage 1 or 2 of kidney disease. It provides high-limit protection for a specific period, which is ideal for covering a mortgage or ensuring your children’s education is funded. One of our core values is respecting your privacy during the research phase. You can use our term life insurance quotes tool to see real market numbers without entering your name, email, or phone number. This allows you to explore available rates at your own pace without the pressure of immediate sales calls. For a broader look at how different plans stack up against one another, check out A Complete Guide to Life Insurance Policies.

Permanent and Specialty Life Insurance

Permanent life insurance, including whole life and universal life, offers lifelong protection that never expires as long as premiums are paid. These policies are significantly more complex than term products and require a higher level of medical scrutiny during the underwriting phase. For this reason, we require a direct discussion with every prospect before providing quotes for permanent coverage, disability insurance, or long-term care. We believe in transparency, and the reality is that we need to understand your specific medical history and GFR trends to advocate for you effectively. This direct conversation ensures that the quotes we provide are both accurate and attainable for your specific health profile.

Permanent coverage can be particularly valuable for long-term renal care planning due to its cash value accumulation. To learn more about how these policies function as financial assets, read our guide on Permanent Life Insurance Policies.

For individuals in Stage 4 or 5 CKD, or those currently undergoing dialysis, traditional term or permanent policies may be difficult to obtain. In these specific situations, Guaranteed Issue policies serve as a vital safety net. These plans are designed to provide final expense protection without the need for medical exams or health questions. While the coverage amounts are typically lower, they ensure that every applicant can secure a level of protection to ease the financial burden on their loved ones, regardless of their kidney health.

Preparing Your Application: A Kidney Patient Checklist

Applying for life insurance with kidney disease requires more than just filling out a standard form. To get the best results, you should treat the application like a professional presentation of your health. Gathering your data beforehand prevents common delays and the risk of “trial” denials, where an underwriter rejects a case simply because the medical picture is incomplete. When you’re ready to start, we recommend having your most recent lab work from the last 6 to 12 months in front of you.

Make sure you have these specific readings ready for your discussion with an agent:

- GFR (Glomerular Filtration Rate): This is the primary indicator of your kidney function stage.

- Creatinine levels: Underwriters look for stability in this number over time.

- Microalbumin or Protein/Creatinine ratio: This helps determine if there is active kidney damage.

You’ll also need a complete list of medications, including dosages for blood pressure management or diuretics. Underwriters will ask for the exact date of your original diagnosis and details on any surgical history, such as biopsies or stent placements. Having this information organized shows the carrier that you’re proactive about your health management.

Medical Documentation You Should Have Ready

Keep a clear list of your medical providers, including your primary care physician and your nephrologist. The Attending Physician’s Statement (APS) is the critical document underwriters use to verify your stability and confirm the medical history you provided. Because requesting these records can take time, having your doctor’s contact information ready speeds up the process significantly. We use these records to advocate for you as a prospect, ensuring the insurance company sees the full context of your care.

Lifestyle and Secondary Health Factors

Lifestyle factors play a massive role in your final rate. Smoking status is a major multiplier; smokers with CKD face significantly higher premiums than non-smokers. Your Height/Weight (BMI) also acts as a secondary health marker. A healthy BMI can help offset a slightly lower GFR by showing the underwriter that you’re managing your overall cardiovascular health. Transparency is always the best policy during this process. Being upfront about your specific CKD stage is far better than letting an underwriter discover it through a surprise blood test during a medical exam.

We believe in making the quoting process as transparent as possible. If you are looking for a term life policy, you can explore anonymous term life insurance quotes right now without sharing any personal data. However, for products like permanent life insurance or disability insurance, we require your contact information first. A direct discussion is necessary to ensure we provide an accurate quote based on the specific medical details you’ve gathered. Reach out to us today to start your application with an expert guide on your side.

How LifeInsure.com Helps High-Risk Applicants

Searching for life insurance with kidney disease often feels like an uphill battle. Many applicants encounter “captive” agents who only represent one insurance company. If that specific carrier has strict renal guidelines, those agents have no choice but to issue a denial or an unaffordable rate. We operate as an independent brokerage to solve this problem. We shop dozens of top-rated carriers to find the ones that view your health stage through a more lenient lens. Our focus is on finding “kidney-friendly” carriers that value your commitment to managing your condition.

Our technology is built around your comfort and privacy. We believe you should be able to research your options without feeling pressured to share personal data immediately. If you’re looking for term life insurance, you can explore rates anonymously on our platform. This allows you to see the market landscape before you decide to move forward with a formal application. We believe every prospect deserves a transparent explanation of their options without the fear of being “put on a list” for marketing calls.

The Advantage of an Independent Broker

Captive agents are often limited by corporate underwriting manuals that don’t account for individual medical nuances. By contacting our team, you gain access to specialists who know which carriers are currently offering the best table ratings for CKD patients. We act as your advocate. We present your case to multiple underwriters to secure the most competitive offer available. This personalized assessment is the most effective way to navigate the complexities of high-risk medical underwriting. Our professional longevity in the industry allows us to know exactly which doors to knock on for your specific health profile.

Setting Clear Expectations for Complex Quotes

While we offer anonymous quotes for term products, complex financial tools require a more personal touch. We require your contact information upfront for disability insurance, long-term care, or permanent life insurance quote requests. A direct discussion is the only way to ensure accuracy for these products. Every prospect has a unique health story. We need to understand the details of your GFR and treatment history to give you a quote that won’t change later in the process. This consultative approach ensures that we accurately represent your health to the carrier. We prioritize your data privacy to ensure a stress-free experience from start to finish.

Take the Next Step Toward Financial Security

Securing life insurance with kidney disease is a manageable goal when you have the right data and an experienced advocate on your side. You’ve seen that your GFR and creatinine levels are the primary drivers of your rating, but your consistent commitment to health stability is what truly matters to underwriters. We’re here to simplify this journey by shopping over 40 top-rated carriers across all 50 states to find your best fit.

Our process is designed to respect your privacy and your time. You can explore term life options privately using our digital tools. If you require a more complex product such as whole life, disability insurance, or long-term care, we’ll ask for your contact information to begin a direct discussion. This consultative approach allows us to accurately represent your unique health profile as a prospect to potential insurers. We provide the expert guidance needed for high-risk medical conditions like CKD.

Ready to see your options? Get an Instant, Anonymous Term Life Quote today. You don’t have to navigate these complex requirements alone, and we’re ready to help you protect your family’s future with confidence.

Frequently Asked Questions

Can I get life insurance if I am on dialysis?

Yes, you can still obtain coverage, though your options are generally limited to guaranteed issue life insurance policies. Traditional term or whole life policies typically aren’t available for those currently on dialysis. These specialized plans don’t require medical exams or health questions, making them a reliable safety net. They usually feature lower coverage limits and a graded death benefit, ensuring your beneficiaries receive protection for final expenses regardless of your health status.

How does a kidney transplant affect my life insurance eligibility?

A kidney transplant doesn’t permanently disqualify you from coverage, but most carriers require a waiting period of 12 to 24 months post-surgery. After this period, if your condition is stable and there are no signs of organ rejection, you may qualify for standard or mildly substandard rates. We find that underwriters look for consistent lab results during this time. Once you reach this stability, we can help you explore both term and permanent options.

Will my life insurance premiums increase if my kidney disease progresses?

No, your premiums will remain the same as long as your policy is active and you’ve locked in your rates. Once a carrier issues a policy, they cannot increase your costs or cancel your coverage because your health changes. This is why we encourage every prospect to secure life insurance with kidney disease as early as possible. Locking in a rate while your GFR is higher protects your family’s budget against future health declines.

What is the best type of life insurance for someone with Stage 3 CKD?

Term life insurance is often the best choice for Stage 3 patients because it offers the most affordable high-limit protection. If your GFR is stable, many carriers will offer a “table rating” that keeps premiums manageable. For more complex needs like whole life or disability insurance, we require a direct discussion to review your nephrologist’s notes. This consultative approach ensures we accurately represent your stability to carriers before you submit a formal application.

Can I get life insurance with no medical exam if I have kidney disease?

Yes, simplified issue policies that skip the medical exam are available for those with mild or well-managed kidney disease. These carriers use your prescription history and medical databases to evaluate your risk. While these plans offer speed and convenience, they may have slightly higher premiums than fully underwritten policies. We can help you determine if a no-exam policy is the right fit or if a traditional exam would result in a better rate.

How long do I have to wait after a kidney surgery to apply for insurance?

The waiting period depends on the surgery type, with minor procedures requiring 3 to 6 months and major surgeries like transplants requiring up to 24 months. Underwriters want to see a full recovery and stable lab trends before committing to a policy. Applying too soon after a procedure often results in a “postpone” decision. We recommend gathering your follow-up lab results first so we can present a strong case to the insurance carrier.

Does Polycystic Kidney Disease (PKD) count as high-risk for life insurance?

Yes, PKD is considered high-risk because it is a progressive genetic condition that underwriters monitor closely. Eligibility depends on your current kidney function and whether you have secondary issues like high blood pressure. Because PKD cases are unique, we require your contact information upfront to provide quotes for permanent or disability products. A direct discussion allows us to advocate for you by highlighting your proactive management and stable health markers.

What happens if I am denied life insurance because of my kidney function?

A denial doesn’t mean you’re uninsurable; it often means that specific carrier wasn’t the right match for your health stage. We can review your denial letter and help you pivot to a carrier with more lenient renal guidelines or a guaranteed issue policy. Since we work with dozens of carriers, we can often find an alternative path for prospects who have been rejected elsewhere. We’ll work closely with you to find a viable solution.

Last Updated on May 20, 2026 by Richard Reich